Weekly Market Update: Calm, Chill Even

In this week's crypto market update, we observe calm in the markets, with the biggest news being a disruption involving Bitgo, Metamask's credit card launch, and economic updates showing mixed signals globally.

After a few weeks of chop, this week has felt relatively calm, chill even. It’s summer holiday season in the north, which generally means markets take something of a breather.

Because of that, and the fact we are between big Fed announcements, it’s been a relatively quiet week newswise. The biggest event seems to be a kerfuffle with Bitgo, the wrapped Bitcoin (wBTC) custodian. Whatever they proposed, markets didn’t like it and a bunch of competitors came out of the woodwork.

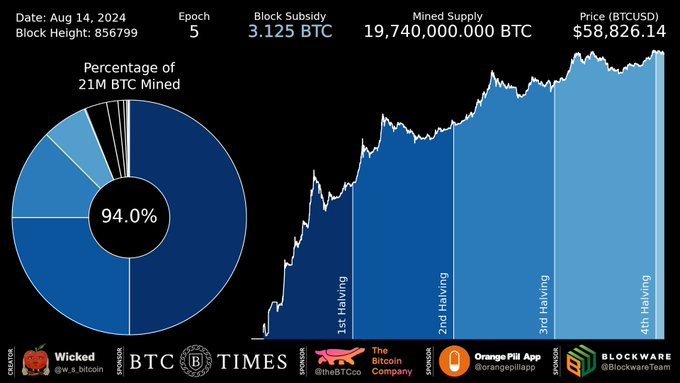

In other news, 94% of all BTC has been mined, Metamask is launching a credit card, Apple is opening up its NFC chip to other payment providers and Aribtrium has voted to allow staking. Also watch out for misinformation, we are in an election year!

In macro market news, commodities like steel are way down due to lower Chinese demand from their cooling housing sector.

Turning to the US; July’s CPI print was good news for the Fed while other indicators seem to point to the much vaunted soft landing.

In Europe the EU posted a trade surplus, while UK CPI and GDP were both higher than expected.

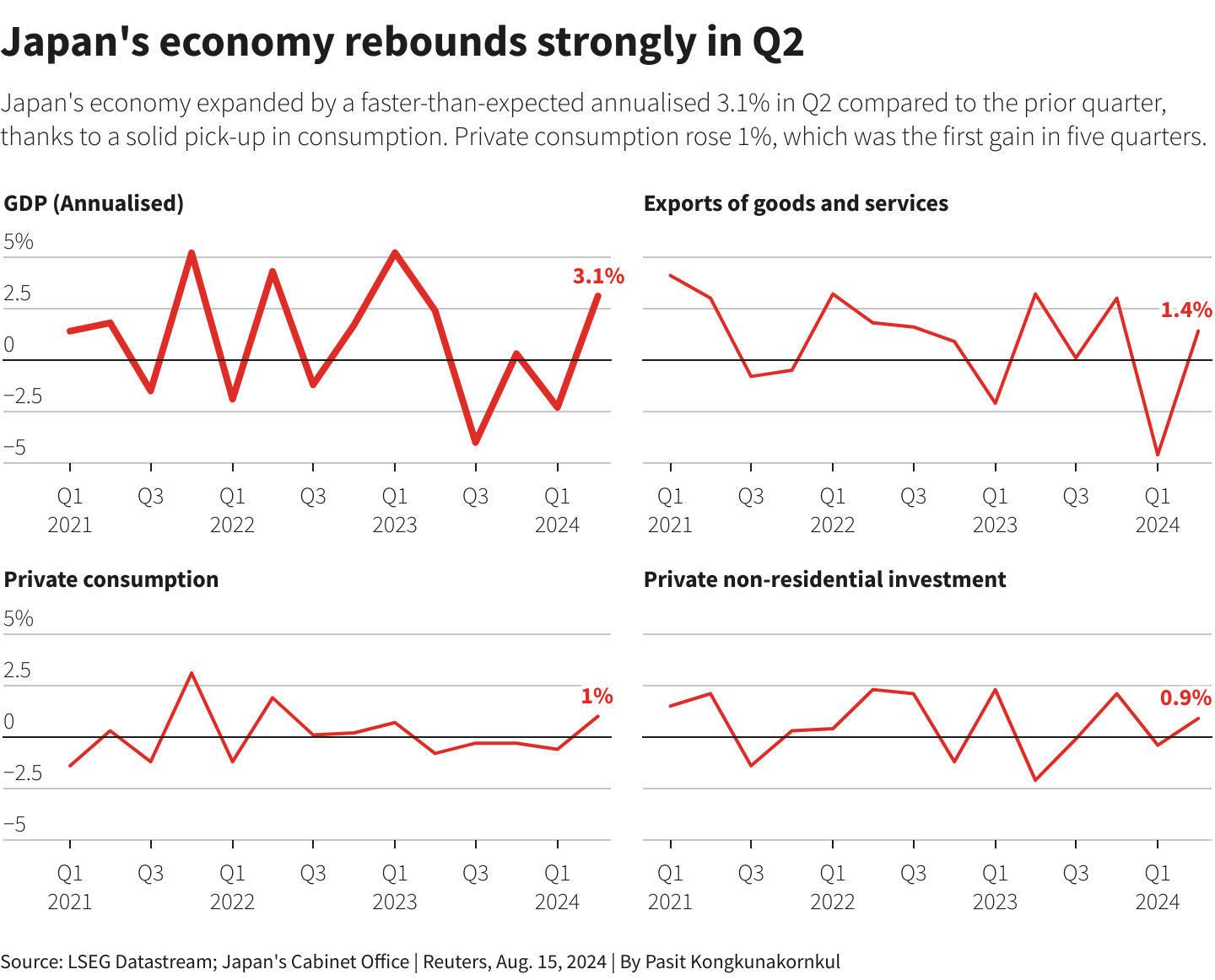

Regionally China’s industrial production and foreign investment continues to fall. Japan’s Q2 GDP was significantly better than estimates and other central banks are starting to cut rates.

Australia may be an outlier, as they added a bunch of jobs. The RBA is definitely hawkish and this is raising the spectre of them being one of the few central banks to be raising rates while others are cutting. Rate differentials people!

In New Zealand card spending continues to trend down as does services PMI. However, we got some good news on producer prices and food price increases.

Market sentiment followed price action this week and basically remained unchanged, holding steady at fear.

Highlights this week:

- The 7 day charts look like a 60/40 split of losers versus gainers. In short a mixed bag.

- Our Buy-Sell ratio by order count has trended back towards our normal range, however by Value, you were all net sellers this week. This was driven by sell activity from our higher value customers.

- There was a big shift towards Stablecoin sells, indicating a degree of profit taking or a shift from Alts.

- At the time of writing BTC and SOL were both down ~2%, ETH was down 4% and BNB and XRP were up 9% and 4% respectively.

- AAVE was our best performing asset this week, up 30% after being punished earlier in the month.

- MKR was our worst performer, down 8% this week.

View all top gainers: Visit the top gainers page to find out more.

Highlights from the crypto space

Its S13 filing season and guess what, Goldman Sachs has bought over $400m in BTC ETF stock.

Coinbase called on the SEC to rethink its DeFi regulation plans, calling it irrational.

Something is going on with wrapped BTC (wBTC), it looks like the custodian is relocating and that is causing something of a ruckus. wBTC has $9bn in BTC assets FYI.

In response Coinbase has launched its own wrapped Bitcoin – cbBTC. (wrapped BTC is a way of getting BTC exposure on the Ethereum network- you deposit BTC into a custodian and they issue you an ERC token – kind of like how stablecoins work)

94% of all BTC has been mined…. Let that sink in.

Metamask has launched a card which allows you to spend directly from your wallet. Only available to a select group of EU/UK users at the moment.

Staying with Wallets, Coinbase is giving out grants to those who want to integrate AI (large language modules or LLM) into wallets.

Apple is (finally) opening up the NFC function on its mobiles, this will theoretically enable web 3 wallets to enable transactions. Some people are pointing out some obvious drawbacks, essentially that we aren’t quite ready.

Arbitrium DAO has voted to allow the staking of ARB, gaining 91% approval.

Ethereum and Solana DEX volume is neck and neck.

USDe issuer Ethena looks like one of the big losers from the market correction.

Stablecoin liquidity is at its highest level since 2022. This is seen as a proxy for markets gearing up for another leg up. Liquidity drives liquidity is the common refrain.

There is a bunch of mis-information flying around about potential appointees if the Democrats win with a hint of anti crypto. Just remember, check your sources and we are in an election year.

The SEC has apparently rejected CBOE’s application for a Solana ETF.

🌎 Macro news TLDR: …All eyes on US CPI.

Reflecting very low Chinese demand, commodities like Reinforced Steel are in free fall. This is playing out across multiple elements.

U.S. economic news

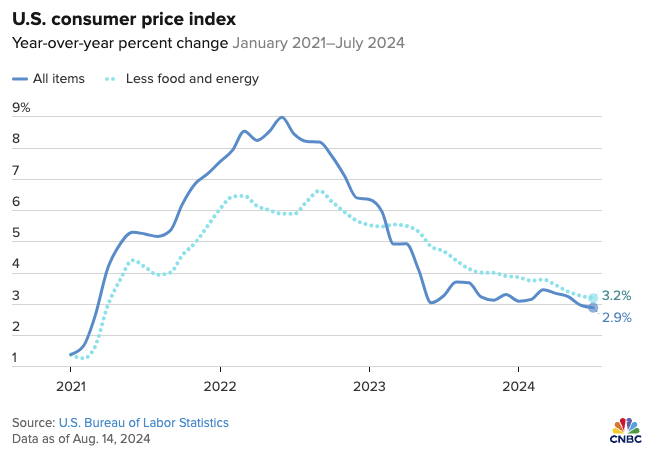

The US July CPI came in marginally under expectations at 0.2% for the month or 2.9% annualised. Core CPI retracted to 3.2%.

This is being seen as the last major datapoint to trigger US rate cuts. Retail Sales continue to perform strongly indicating no consumer recession in sight, they were up 1% in July.

New housing construction fell in July. The Conference Board‘s leading indicators point to a softening economy.

Over in Europe….

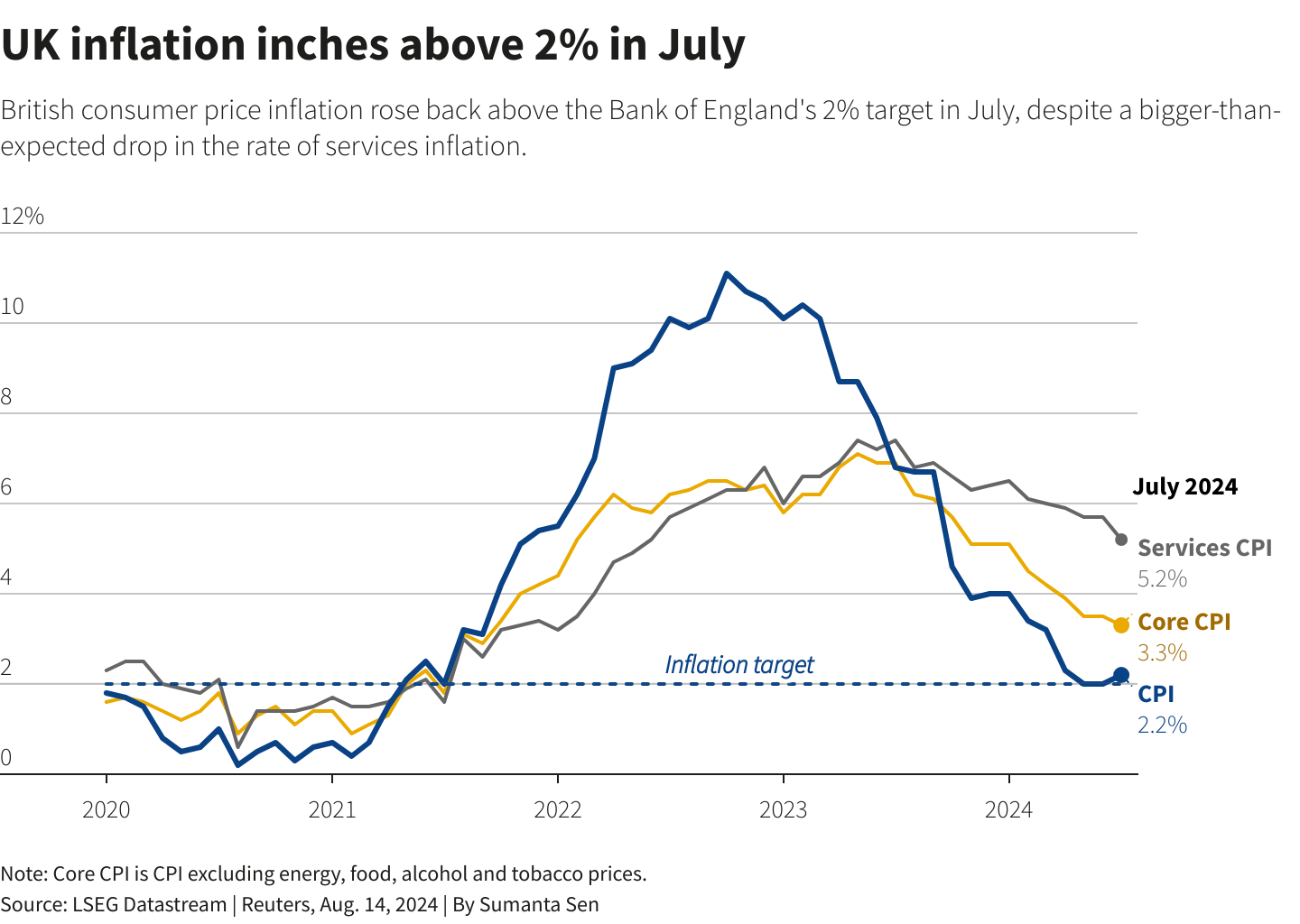

UK CPI increased by 0.2% in July, this is still below the EU. UK Q2 GDP was 0.6% and the indicators are that the economy is starting to hit its straps.

The EU posted a trade surplus, mainly because imports were down over 9%. German producer prices are still down, August at -0.8% hinting at continued deflation.

And in Asia Pacific…

China’s industrial production fell for the 3rd straight month to be 5.1% in July. Foreign Direct Investment has been tanking in China, for the year to July it’s down 29%.

The PBOC held rates steady as expected. Japan smashed Q2 GDP expectations by a full percentage point, coming in at 3.1%, vs the forecast 2.1%.

Philippines Central bank cut rates to 6.25%, its first cut since 2020.

In Australia, unemployment ticked up to 4.2%, however they added 40,000 jobs and the uptick in unemployment was due to a big increase in the participation rate.

Not quite what the RBA wanted to see and that came through in their minutes which are rightly hawkish and show an increased worry inflation is not turning.

In New Zealand, electronic card transactions fell for the 6th month in a row, with volume declining 0.1% in July. Food prices increased 0.6% for the year.

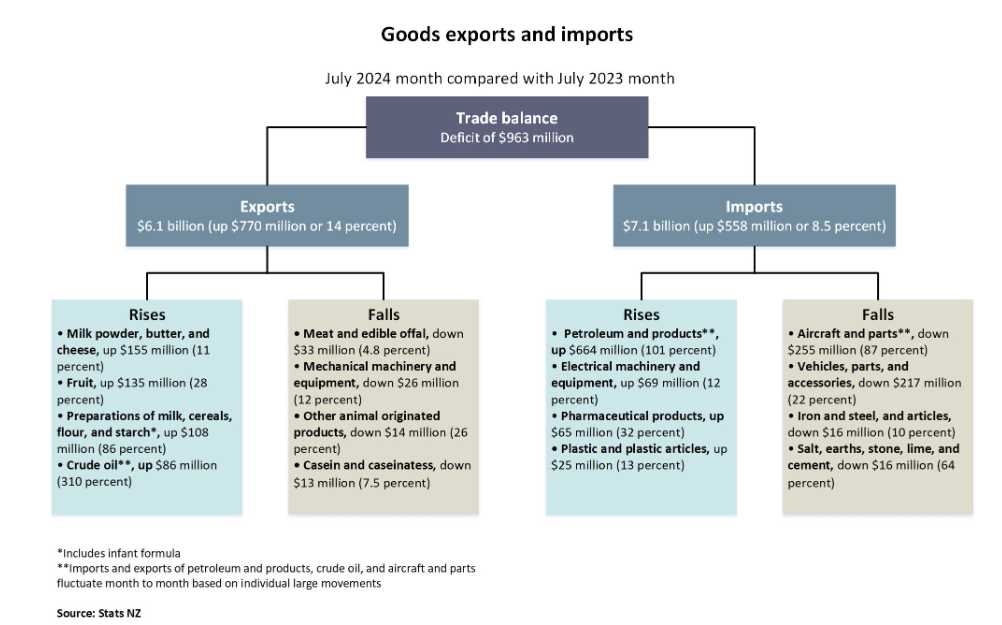

NZ Producer prices increased 1.1% in the June quarter. Services PMI fell for the 4th straight month recording its lowest, non Covid result on record at 40.2. In the year to July we posted a trade deficit of $963m.

That’s a wrap for this week.

Stay tuned for the next update.

Did you miss the last weekly update?

Share to

Stay curious and informed

Your info will be handled according to our Privacy Policy.

Table of Contents

We make it easy.

Start your crypto journey today!

Make sure to follow our Twitter, Instagram, and YouTube channel to stay up-to-date with Easy Crypto!

Also, don’t forget to subscribe to our monthly newsletter to have the latest crypto insights, news, and updates delivered to our inbox.

Disclaimer: Information is current as at the date of publication. This is general information only and is not intended to be advice. Crypto is volatile, carries risk and the value can go up and down. Past performance is not an indicator of future returns. Please do your own research.

Last updated August 21, 2024