Weekly Market Update: Ramp Up in Institutional Interest

In this weekly market update, we take a look at the recent market activities with institutional players in the space. Stay tuned for other macro economic developments around the world.

It’s been a relatively benign week in the markets this week with most suggesting that we are holding our breath for the US rate decision delivered later this week.

The odds are heavily weighted towards no change this month. However, increasing inflation driven, mainly by the rising cost of oil, means the chance of a rise next month is increasing.

This week a number of top tier banks announced well progressed blockchain and crypto projects. Looking back over the last 6 weeks it would be hard for anyone to argue that this trend is not real.

Crypto winters are for building and there were also a number of great new product releases announced. Great to see the builders getting their stuff out!

In the wider macro economy, both the US and EU appear to be getting toward the end of their central bank hiking cycles.

The US inflation picture was mixed, mainly due to energy (oil) and housing with the threatened shutdown adding to an already uncertain picture.

While Europe seems to be slightly more negatively affected due to its larger dependency on global trade.

In Asia, China finally got some good news, while India and Japan continue to post good numbers. Australian Business confidence is up, while in New Zealand our Manufacturing and Service PMI’s are still retreating.

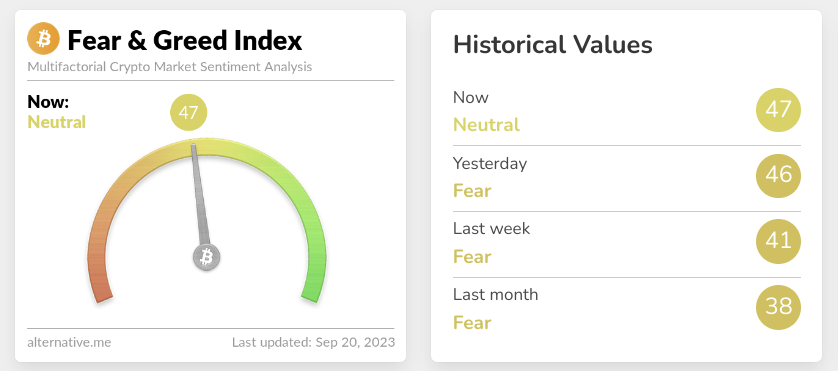

The market sentiment remains in fear territory this week, but has improved significantly from last week’s FTX FUD sell down.

Trend highlights this week:

- What a difference a week makes! A quick glance at the top 30 assets shows a soothing array of green on the weekly charts.

- BTC and ETH are up 4% and 2% respectively

- Thorchain (RUNE) was the best performer this week, up 27% on the Metamask / Shapeshift news.

- Stellar (XLM) was our worst performing asset, down 3.6%.

View all top gainers: Visit the top gainers page to find out more.

Looking for more flexible pricing and trading volume for your high-value crypto trades? Get in touch on our OTC page and learn how we can help.

Highlights from the crypto space

Metamask has introduced a new feature called Snaps which is basically an app store. One of the apps is shapeshifter so you can now have native BTC (not wrapped) in Metamask. 🤯

Telegram, in partnership with TON, is also launching a non-custodial wallet.

SEC chairman Gensler is frontrunning his testimony to the House oversight committee by saying there is wide ranging non-compliance in crypto.

And it looks like some key members of the Democrats are liking his approach. The SEC however is not having it all its way, with a Federal Judge ruling that they can’t get immediate access to Binance US software.

There are reports that HSBC is working with Fireblocks for custody. JP Morgan is looking to blockchains to deliver efficiencies in financial services. So too are Citigroup who have developed their own permissioned blockchain.

Charlie Bilello has been at it again with those pesky comparisons.

Zero Knowledge (ZK) rollups are coming to the Bitcoin network. TLDR on the benefit; the potential to make the blockchain more efficient while maintaining security.

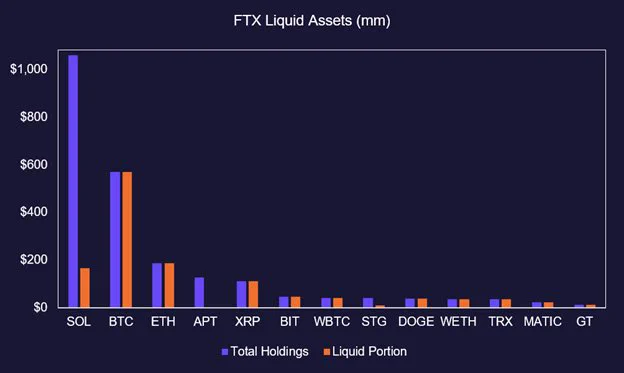

Following on from last week’s FTX FUD, which made SOL holders in particular feel pretty exposed, someone has analysed the liquid parts of the holdings. 👇 TLDR, don’t panic

Other notable highlights from around the crypto space:

- NASDAQ has joined the EFT wave, however their filing is different as its a mixed spot/futures ETF.

- Commenting on this wave of ETF applications, Morgan Creek Capital’s Mark Yusko came out and said that Bitcoin is on sale at the moment.

- Mountain Protocol has launched a new US denominated stablecoin – USDM. Using a mechanism similar to Lido’s stETH token, you will get paid daily rewards derived from US treasuries for just holding the coin. It is definitely a security so not available to US persons.

- In the wake of the SEC actions against Binance US. The CEO has resigned, they have also made one third of the staff redundant.

- Genesis, a subsidiary of DCG, will cease offering any crypto trading due to business reasons. DCG also put forward a payment plan for the $3.5bn they owe. Gemini’s lawyers are unimpressed, calling it misleading at best.

- Paypal partner Paxos overpaid on a BTC transaction to the order of 500k USD. They are trying to get the fee back.

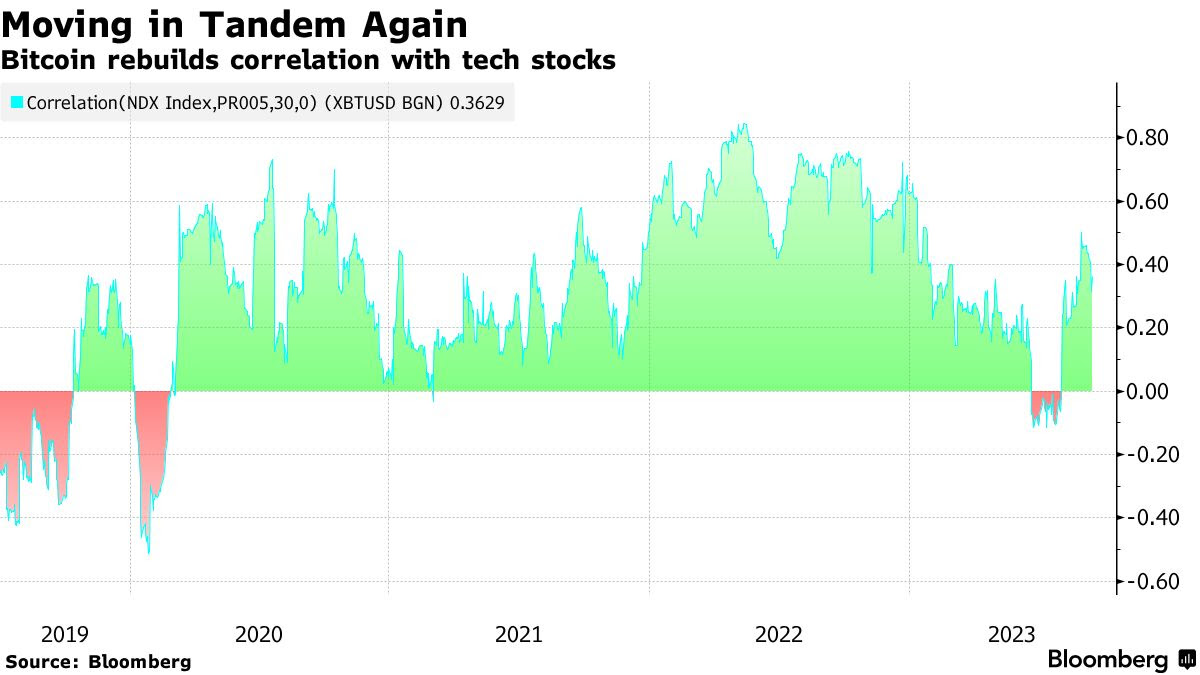

- Bitcoin’s correlation with Tech stocks has risen significantly since June as the Nasdaq has risen on the back of AI hype / exuberance.

- North Korea’s Lazurus hacking group appears to be stepping up its activity and seems to be particularly focused on centralised venues.

And that sums up the major updates from around the crypto space. Moving on, we’ll take a closer look at other macroeconomic developments from around the globe.

Starting off with global news

Global oil prices continue to rise, with Brent Crude flirting with $95 a barrel due to concerns over constrained supplies. These costs are already showing through in broad CPI and PPI figures globally.

Global shipping giant Maersk, has said that there are tentative signs of a pick up in global trade underway as shipping volumes are picking up.

🌎 Macro news TLDR: Markets waiting on US Fed funds rate.

The EU is threatening China’s EV industry with tariffs to stave off a flood of imports.

Cynics are questioning if this has something to do with the struggles of the massive EU auto industry. On top of this, the EU has warned that they could become as dependent on China for Lithium Batteries as they are on Russia for gas.

Argentina has decided to hold its interest rate at 118%, there is concern inflation could rise to 168% pa. Crypto anyone?

U.S. economic news

Rinse, repeat. The threat of another government shutdown has returned with government funding approved only to September 30th. As per usual, there is a standoff between parties.

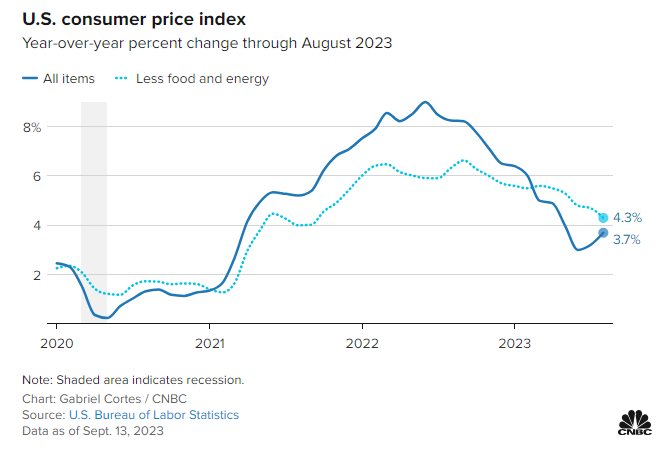

Last Thursday, the US CPI data for August came out with it increasing to 3.7% from July’s 3.2%. This was slightly up on the 3.6% estimated, however Core CPI (excluding food and energy) came in as expected at 4.3%.

It’s the lowest Core CPI reading in 2 years. Outside of energy, increasing housing costs were largely blamed for the increases. Markets pretty much shrugged off the news.

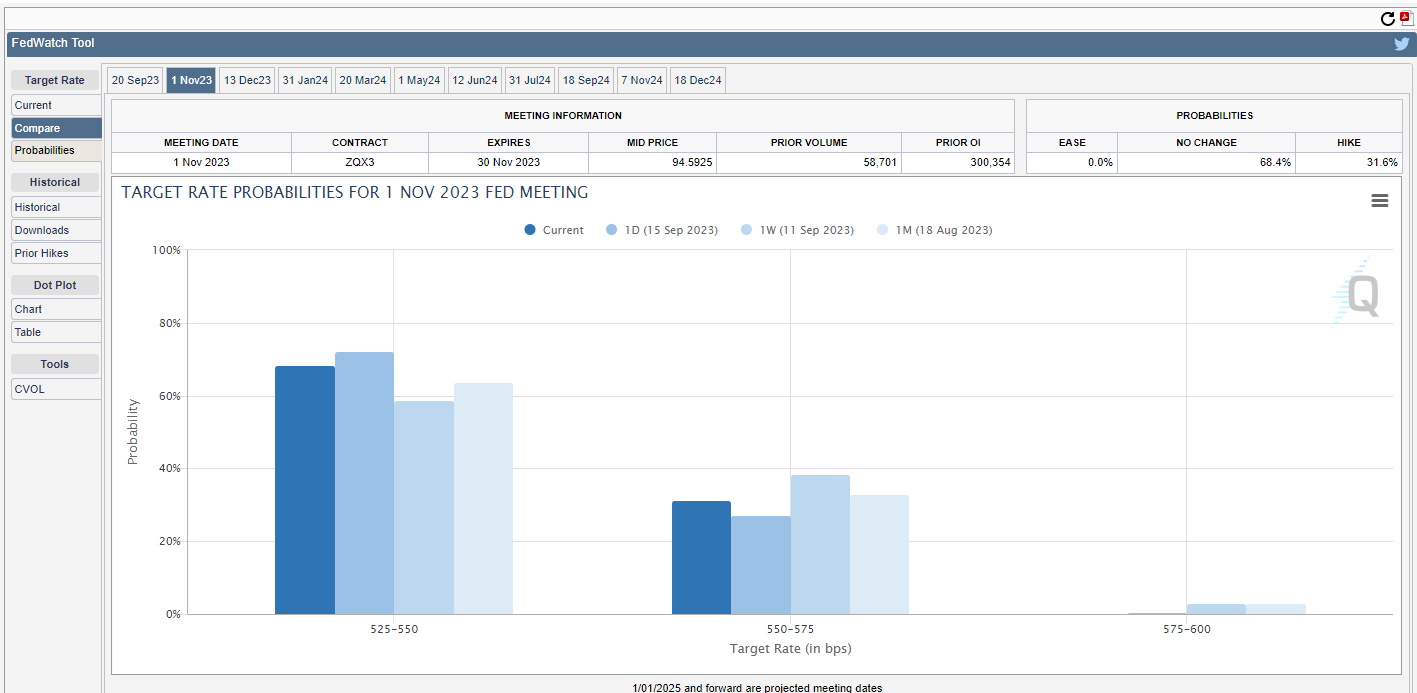

What does this mean? 97% of the market are predicting no rise in interest rates at this Thursday’s FOMC meeting, and the chances of a rise in the November meeting are flat according to the CME Fedwatch predictor.

A union representing 146k auto workers, the UAW is set to strike against all three Detroit auto manufacturers. There are fears that the scale of this industrial action, which represents 3% of GDP, will have national impacts.

And in Europe….

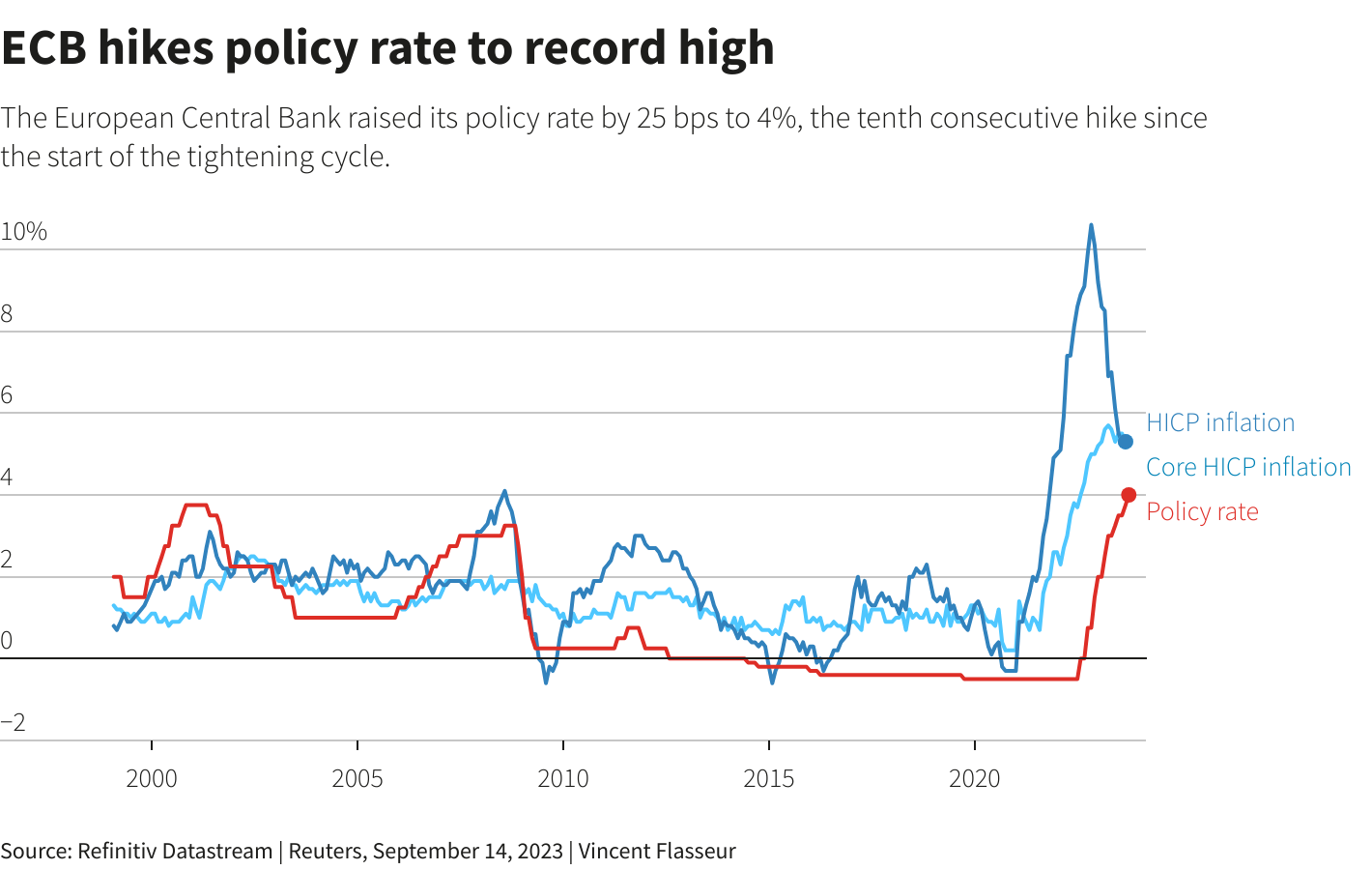

The ECB raised its key interest rate to 4%, a record high. It also said that this is likely the last rate rise in this cycle. They also pushed out their timeline to return to their 2% target. Higher for longer baby.

Wage growth in the UK is running at 8.5% annualised and appears to still be going up. Even with such steep increases, earners are just getting ahead on an inflation adjusted basis.

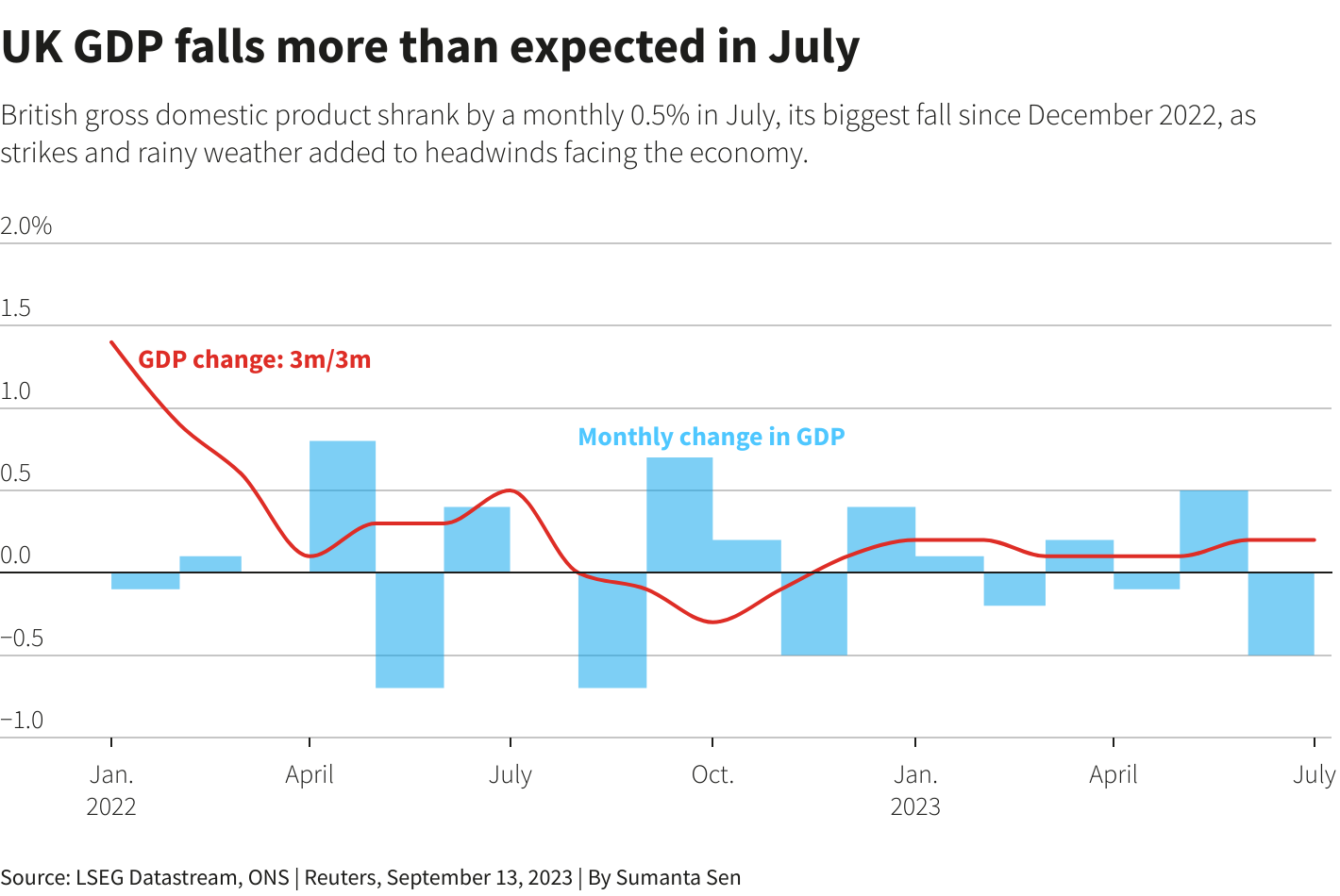

Unemployment is starting to trend up too. GDP in the UK was way down in July, declining 0.5% with the finger pointed at industrial action in the health and education sectors.

Sweden has been battling a property slump too with one of their largest developers in trouble which in turn is impacting one of the largest pension funds to add to the woes.

Russian inflation is picking up and the Russian central bank is raising interest rates to 13% to keep a lid on inflation and defend the Ruble.

And in Asia Pacific…

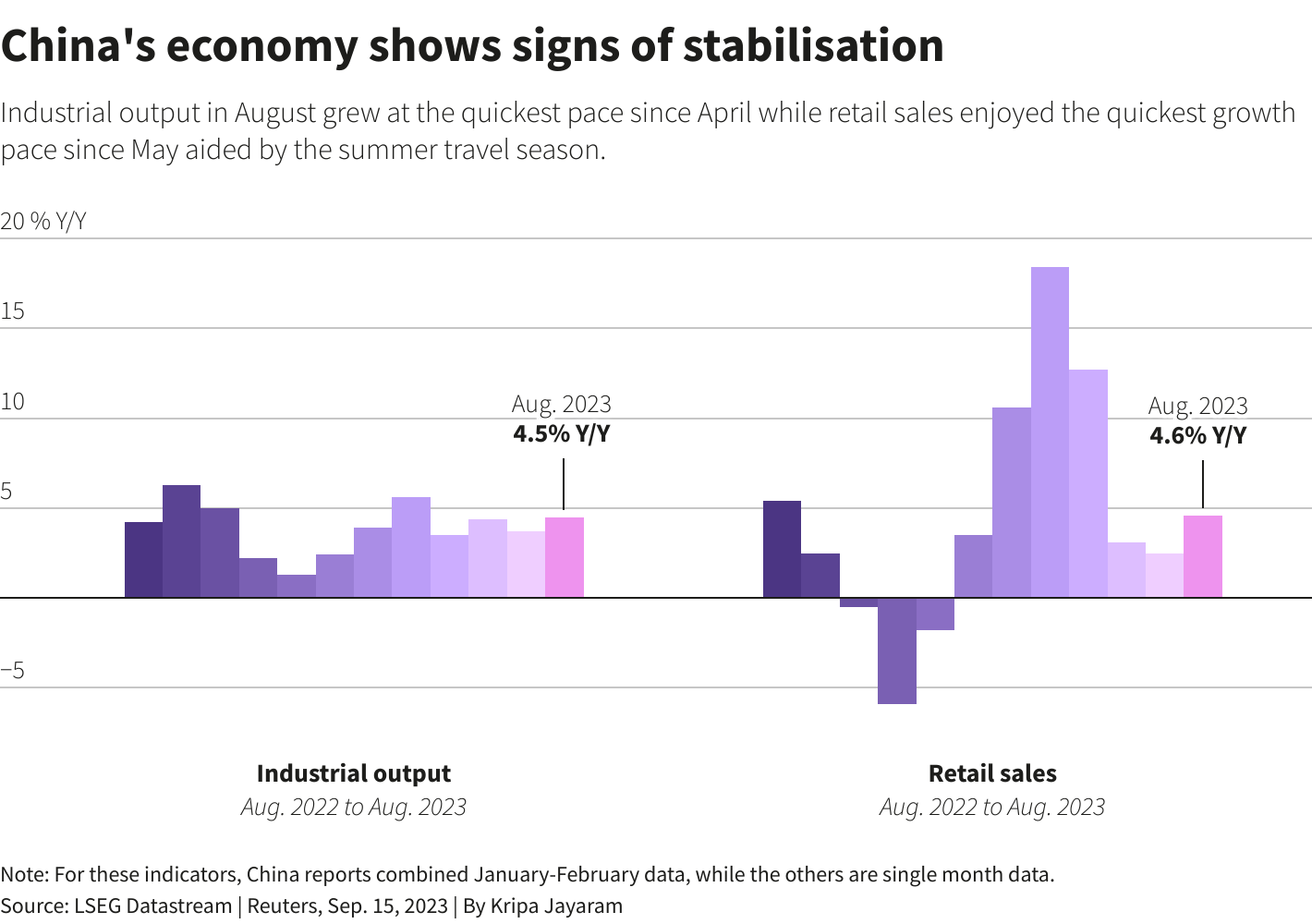

China has managed to halt the negative trends with both factory output and retail sales up in August. It’s too early to say the slump is over, particularly as their property sector is still a festering sore.

India’s CPI data for August showed a modest decline to 6.8% from the 7.4% reported in July. Industrial production continues to rip, coming in a full 1% over estimates at 5.7% for the year.

Japan’s producer prices for August beat expectations at 0.3%. South Korea’s unemployment rate fell to 2.4%.

In Australia, the Westpac-Melbourne Institute Consumer Sentiment index is still falling. Business confidence edged up over the same period.

Meanwhile in New Zealand, the Food Price Index reported an annual increase of 8.9% for August, marginally better than July’s 9.6%.

With immigration running hot, it’s no surprise to find that house prices have started to rise, REINZ data showing we are 2.1% from the bottom nationally.

The latest BNZ BusinessNZ PMI survey showed we are still contracting with August’s number being 46.1, down on July’s 46.6. Services PMI was also down, coming in at 47.1.

That’s a wrap for this week. Thanks for reading!

Stay tuned for the next update.

Did you miss the last weekly update? Catch-up on the previous market update.

Share to

Stay curious and informed

Your info will be handled according to our Privacy Policy.

Table of Contents

We make it easy.

Start your crypto journey today!

Make sure to follow our Twitter, Instagram, and YouTube channel to stay up-to-date with Easy Crypto!

Also, don’t forget to subscribe to our monthly newsletter to have the latest crypto insights, news, and updates delivered to our inbox.

Disclaimer: Information is current as at the date of publication. This is general information only and is not intended to be advice. Crypto is volatile, carries risk and the value can go up and down. Past performance is not an indicator of future returns. Please do your own research.

Last updated September 20, 2023