Weekly Market Update: BTC Regains Key Support Level

In this weekly crypto market update, we look at the markets BTC dips to $53k but recovers; Robinhood expands in the US. Rising shipping costs, political shifts in Europe and Asia. Stay tuned for macroeconomic developments from around the globe.

Last week we referenced Ledn’s BTC price predictions which highlighted that if we broke US$56k, we could go lower. Well it seems Mt Gox and the German government were enough to trigger a run to the 53k. A mini fight back has seen us regain the key $56k support level but it’s a close run thing. We may need a catalyst.

Outside of prices, notable crypto news included Robinhood expansion in the US, Consensys acquiring some wallet security and a Bank of America report the younger people favour less traditional investments which supports our own research. We also saw the weirdest move by Celsius.

Also thrown in there was some interesting analysis of airdrops (sell straight away!), and some data suggesting Solana might be about to run.

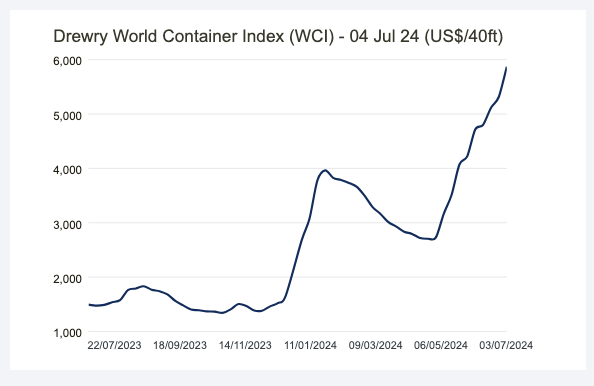

In macro news, there were a number of big elections last week with what looks like a notable shift away from the right in most countries. Also worth noting that shipping costs just keep getting worse and worse.

In the US, the big news story will be the CPI data out later this week. However leading in, their employment data would appear to support an economic softening and could finally bring the Fed around to considering rate cuts.

Chairman Powell said the economy is no longer overheated but reiterated that any cuts are data dependent.

In Europe it was all about politics. The UK delivered a resounding and conclusive result, while Europe’s 3rd largest economy, France looks set for a hung parliament.

In Asia, outside of India, most economies appear to be softening with PMI and Services PMI moving into contraction. Even the lucky country, Australia, looks like it’s slowing.

In New Zealand unemployment is up, while Treasury posted better than expected revenues due to higher tax take from PIE funds. Finally, the RBNZ held the OCR at 5.5% citing domestic inflation as being particularly slow to fall.

While the MPC did acknowledge that financial stress was increasing, and they aren’t as hawkish as May, the no change is going be painful for many.

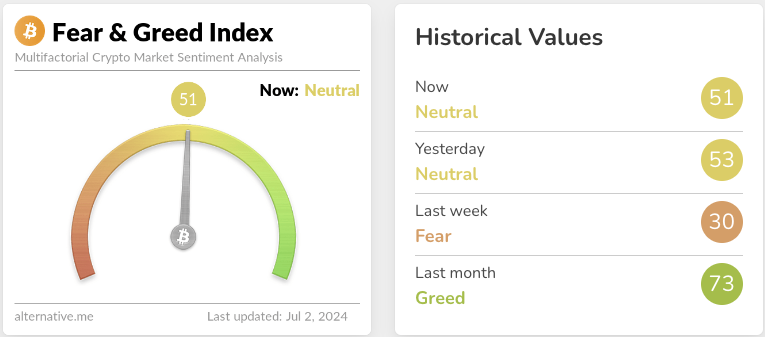

The crypto market sentiment continues its extreme oscillations. We have moved from greed to fear inside of 3 weeks. Probably worth noting that BTC is still up 31% YTD and sitting at US$57k. Wild.

Highlights this week:

- Late last week we saw asset prices dive sharply on what can only be called a sentiment run as traders saw the German government and Mt Gox movements as downside pressure.

- Your response? Buy ! We can only guess that you saw the lower prices as a buy signal as the buy-sell ratio moved significantly to the buy side by order count and value. This skew was even more evident for our higher spending customers.

- BTC was by far the most bought asset, being hovered up at rates way outside its normal range.

- At the time of writing BTC and SOL were both down 6%, while ETH, XRP and BNB were down 10%.

- MultiversX (EGLD) was our best performing asset, up 13% on the week.

- FTM was our worst performer this week, down 23%.

View all top gainers: Visit the top gainers page to find out more.

Highlights from the crypto space

The German Government continues to sell its BTC holdings. They are doing it in a managed way so this is a bit of a ‘sell the news’ story.

Adding to the sell pressure, Mt Gox trustees are starting the distribution of BTC and BCH this month. Despite this, BTC has regained the key support level of US$56k, and even caused a bunch of liquidations when it broke $57k.

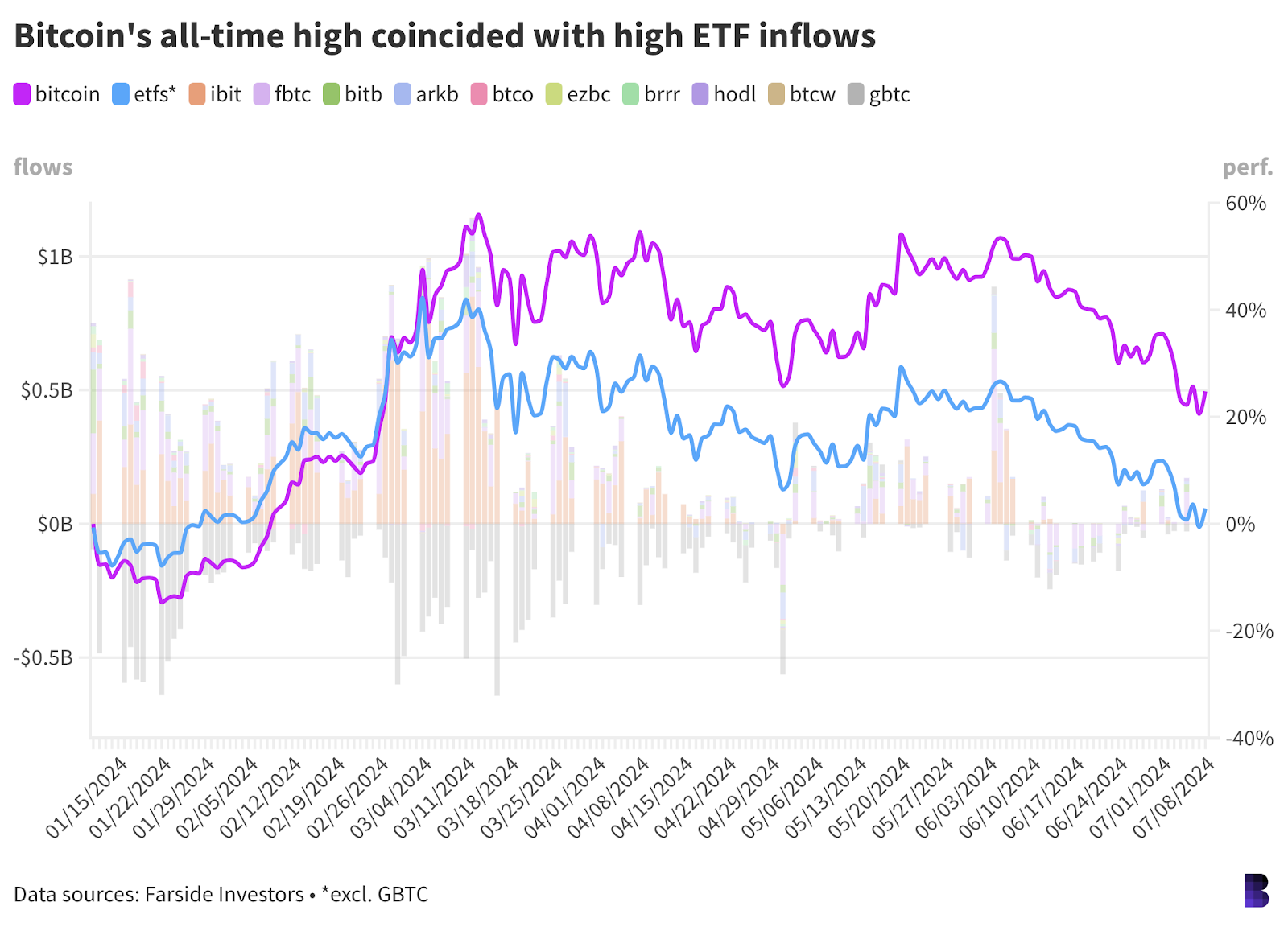

Ever wondered how BTC EFT holders are doing? Us too. Empire put out a piece of research on that today, TLDR; if the blue line is above zero, you made money.

Robinhood is making crypto available to 50 US states.

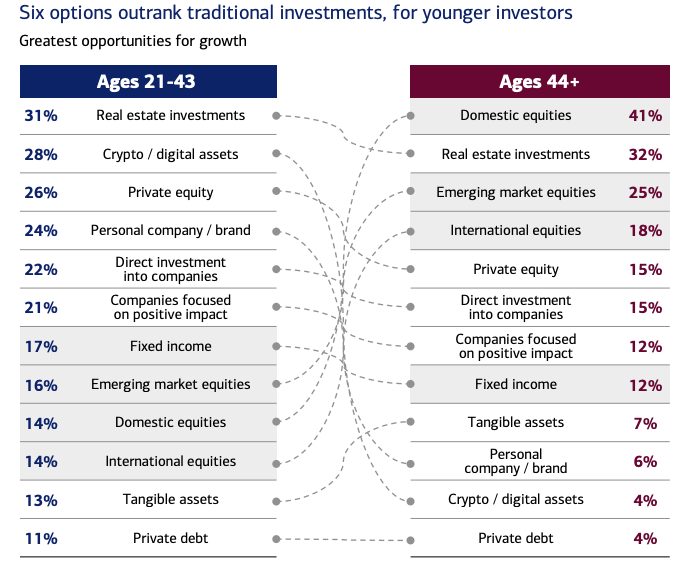

A Bank of America report points to the same trend as our own research. That younger people are sceptical of traditional investments.

Consensys is acquiring Wallet Guard to help users to protect themselves.

The ETH ETFs could come as soon as next week! Polymarket has them lining up for the 26th of July.

An analysis of Airdrops suggests the best strategy is to sell, immediately! Not many hold value.

Two ERC standards are paving the way for stealth addresses, meaning you can send a payment without the end user seeing your entire transaction history. This is seen as important for those who aren’t into radical transparency.

Popular Wallet, Rabby.io is being accused of adding a swap fee by stealth.

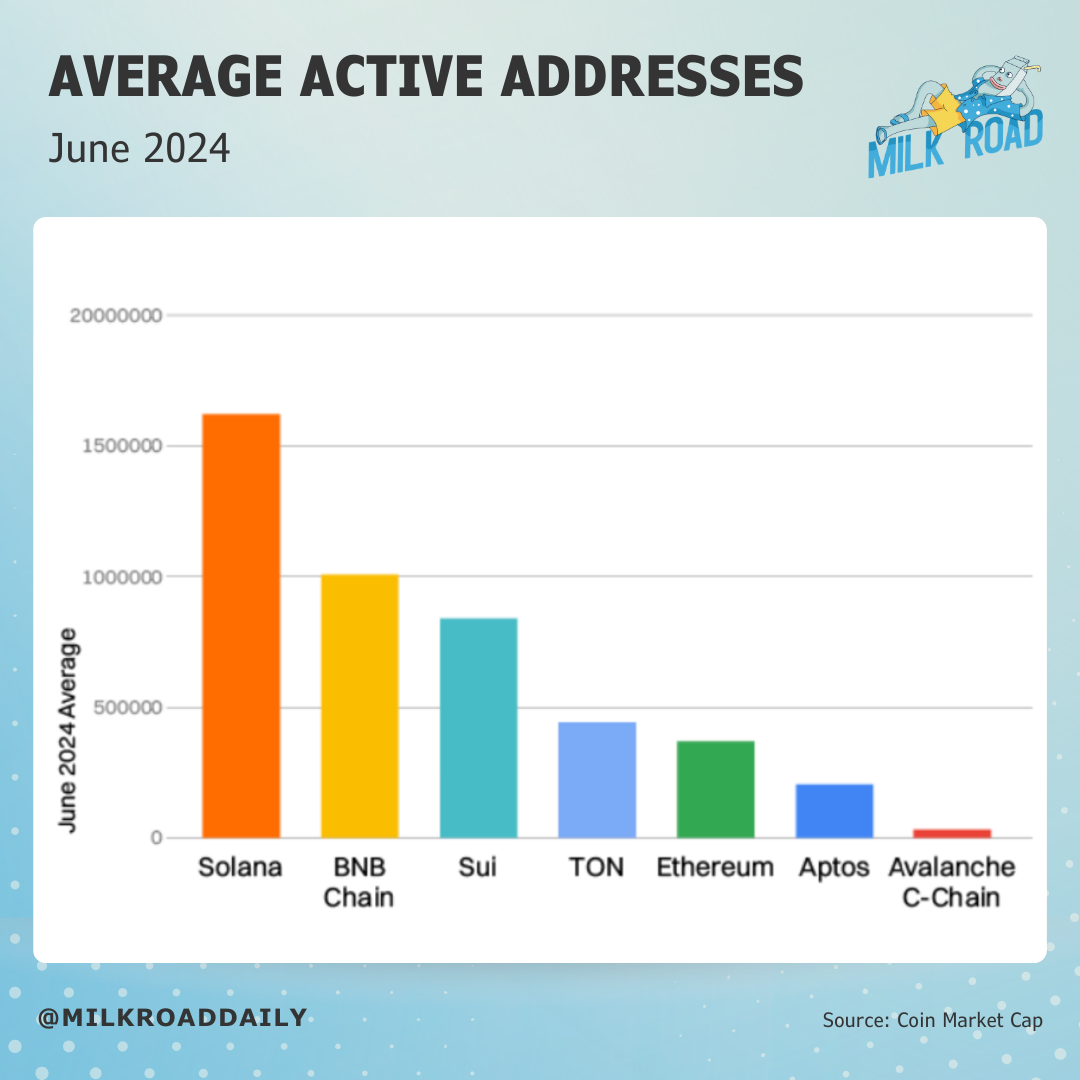

Milk Road is suggesting that the onchain fundamentals could mean that Solana is looking solid for a moon shot (their words, NFA).

There is now a second application for an ASX listed ETF in Australia.

Bankrupt lender, Celsius, is suing its former customers for withdrawing their tokens prior to it going bankrupt. It wants your tokens back, at TODAY’s prices. You read that right.

🌎 Macro news TLDR: …Higher for longer cools markets

We sound like a broken record, Containerised shipping rates continue to increase, up 10% this week. Same root cause.

Not sure where to put this, but a moderate won the Iranian Presidential election, potentially opening up the way for a less confrontational regional play. Maybe.

U.S. economic news

The June minutes from the Federal Reserve meeting show they are happy with the current trend in inflation but they want it to go faster.

The signs of a softening labour market are showing, with unemployment claims up and private job additions down.

This trend was confirmed by the much watched Non-Farm Payrolls report. While more jobs were added (206k vs expected 190k), mostly due to Government headcount (33%!) and health care, unemployment rose to 4.1%. A deep dive into the employment numbers shows things are definitely slowing.

US consumer inflation expectations continue to trend down which could be good news for the CPI data out later this week. It’s now at 3%.

Chairman Powell was grilled by the Senate banking committee on CPI (it’s an election year!!!). He gave little away and simply said the economy is no longer overheated but reiterated that any cuts are data dependent.

Over in Europe….

The EU tariffs on Chinese EV imports hit this Friday.

German factory orders are 8.6% down on last year, and they missed the June estimates by 2.1%. It’s bad.

The Conservatives performed as poorly as forecast in the UK general election. As such the UK has a new government with arguably a large mandate to get the country ‘ back on track’ but a lot of scrutiny as well.

The second vote in the French election delivered another surprise, with the left and centrist coalition appearing to beat out the right after their early round successes.

And in Asia Pacific…

India’s services sector continues to expand with the Services PMI increasing to 60.5 for June. China on the other hand posted a Services PMI decline to 51.2, while Japan’s services moved into contraction at 49.4. There are more concerns about China’s ageing population and the economic headwinds it will bring.

Australia posted a smaller than expected trade surplus of AU$5.7bn. The trend is downwards. As is lending in their housing market, down 2% in the last month.

Australian consumer sentiment remains at very low levels as family finances are under pressure.

In New Zealand, Treasury reports that in the year to May, government income was $1.6bn ahead of forecast due to higher tax take from PIE and investments.

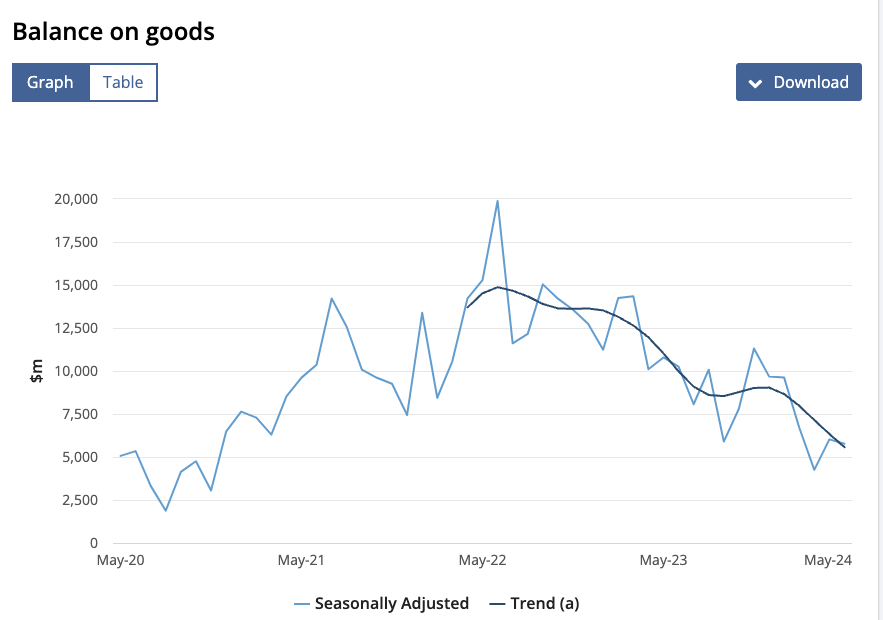

We posted a smaller than expected deficit of $7.7bn. MSD data shows unemployment is up 14,700 for the year to June with ANZ predicting way more to come.

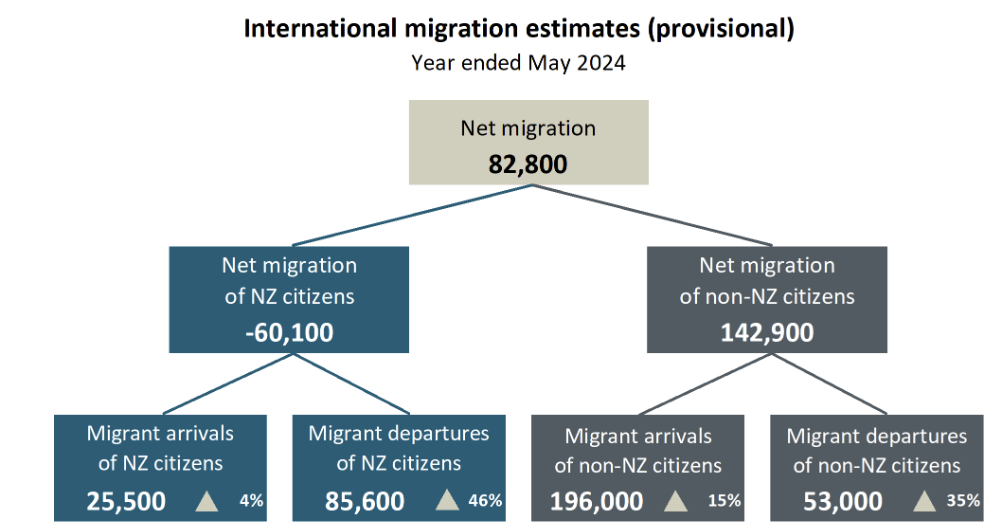

Stats NZ report that net migration in the year to May continues its downward trend, with 83k net migrants coming in.

New Zealanders migrating continues at record levels meaning May 2024 recorded a net population decline of 2000.

Finally the RBNZ monetary policy committee decided that the economy is not in enough pain yet, so held rates at 5.5%. They do so the restrictive stance affecting change and removed any language about a rate hike. How nice.

That’s a wrap for this week.

Stay tuned for the next update.

Did you miss the last weekly update?

Share to

Stay curious and informed

Your info will be handled according to our Privacy Policy.

Table of Contents

We make it easy.

Start your crypto journey today!

Make sure to follow our Twitter, Instagram, and YouTube channel to stay up-to-date with Easy Crypto!

Also, don’t forget to subscribe to our monthly newsletter to have the latest crypto insights, news, and updates delivered to our inbox.

Disclaimer: Information is current as at the date of publication. This is general information only and is not intended to be advice. Crypto is volatile, carries risk and the value can go up and down. Past performance is not an indicator of future returns. Please do your own research.

Last updated July 10, 2024