Weekly Market Update: Germany Ends BTC Sell Off, Crypto Rebounds

In this week’s crypto market update, we look at BTC's positive performance, global adoption grows, and Binance shows strong reserves. Stay tuned for macroeconomic developments from around the globe.

Crypto news was much more positive this week. The Germans have completely sold their BTC bag and a pro(ish) Presidential candidate looks set to take out the US election. The vibes ran positive.

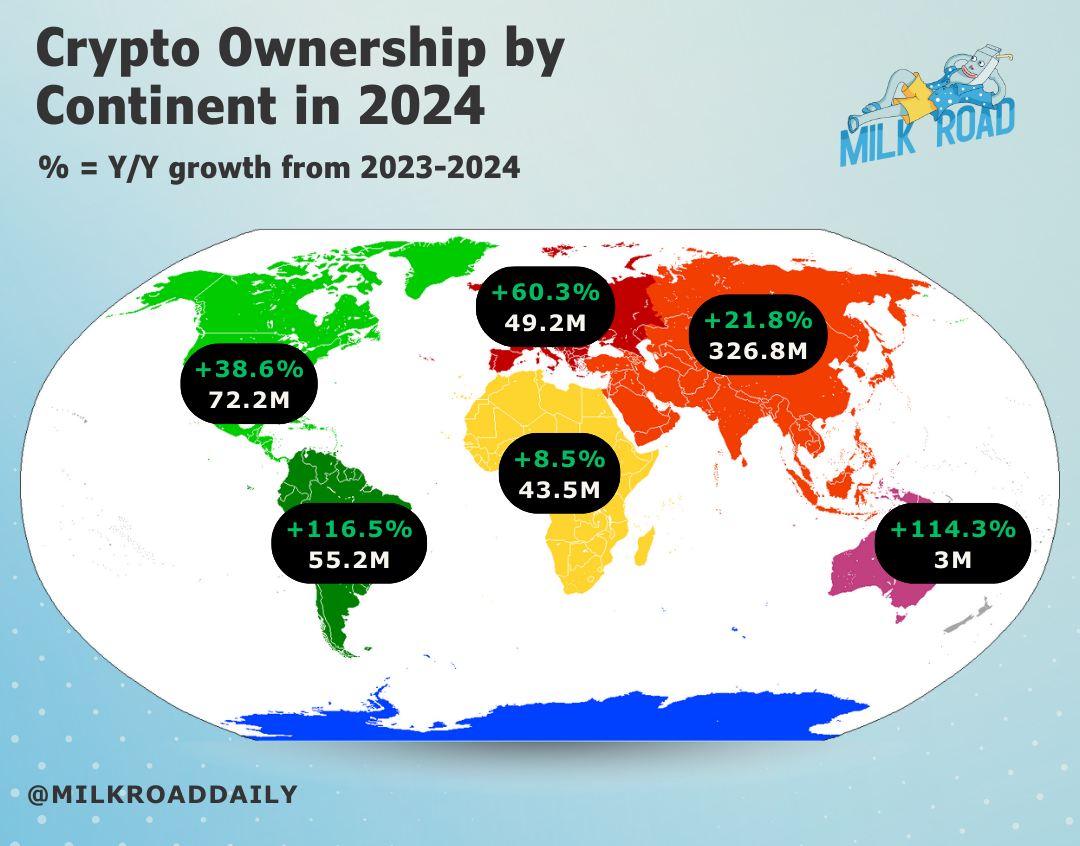

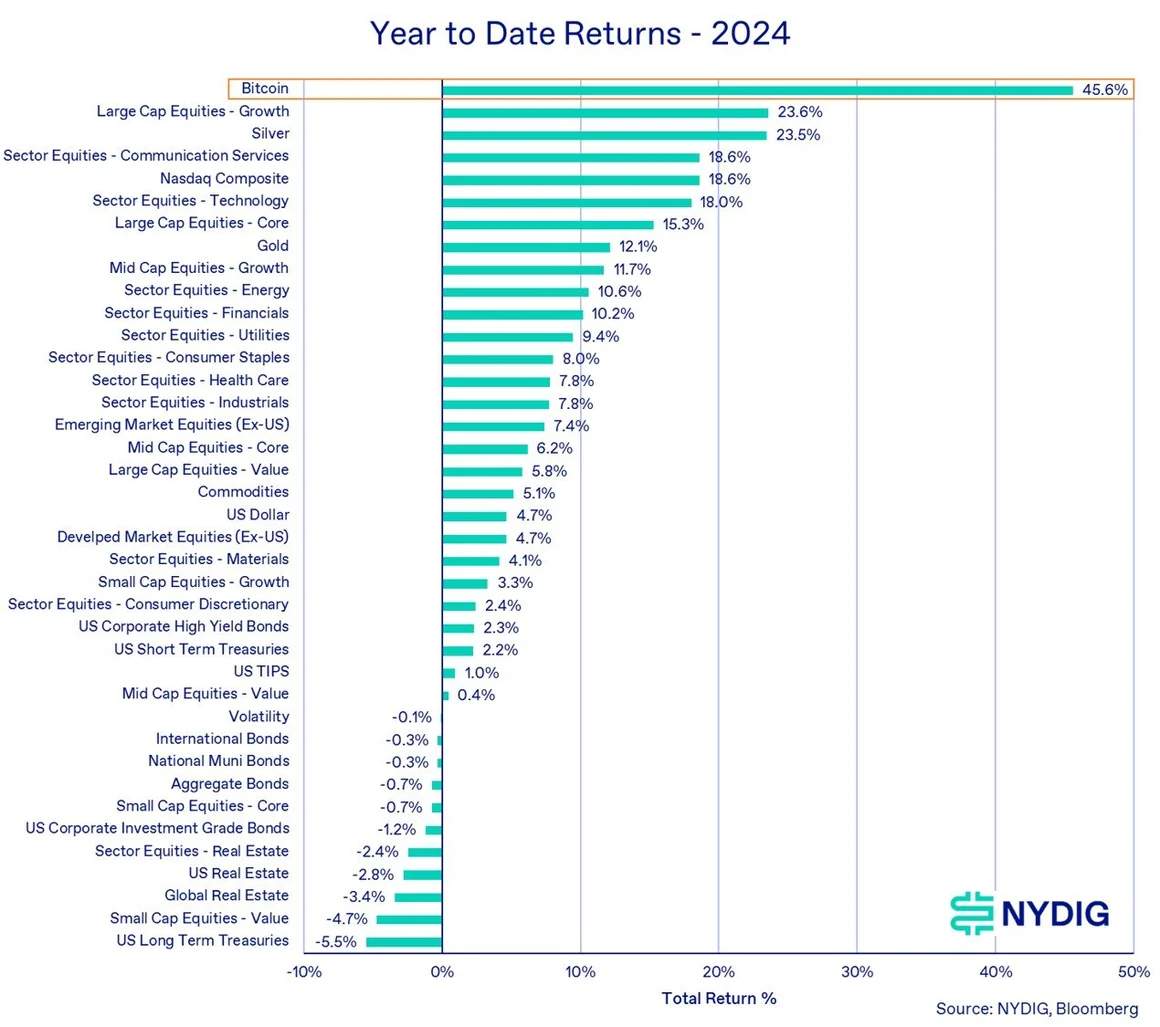

In the crypto news cycle, there is a great report out showing rapid crypto adoption across the world and the Real World Asset space (RWA/Tokenisation) looks like it’s really starting to take off. Binance proof of reserves shows stellar growth, and despite a poor Q2, BTC is still the best performing asset year to date. 💪

In macro news, there is another challenge to the US dollar emerging, while container shipping prices may have plateaued finally,(but prices are still eye-wateringly high!).

The big news this week was a very good CPI reading out of the US showing a month on month decline in headline CPI. PPI (wholesale inflation) was also down. ‘Good news’ said the investors. Markets are further buoyed by the clear shift to Trump as the predicted President following the assassination attempt.

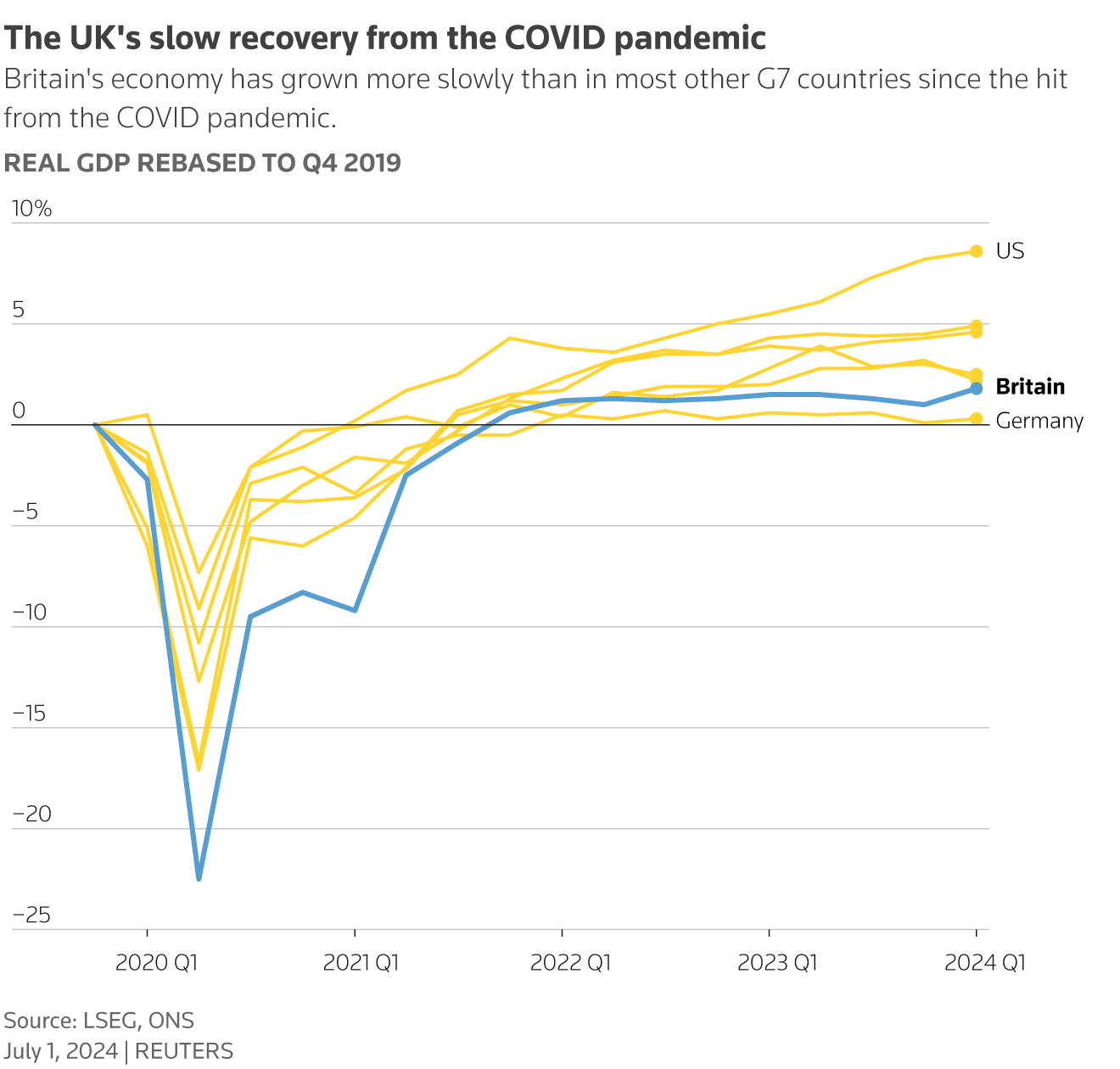

In Europe , German CPI continues to retreat while in the UK their newly minted government got a better than expected GDP result. In context the UK is still a laggard though.

In Asia, China is clearly struggling. CPI was meagre and below expectation and PPI is in negative territory. The anchor that is the property market has also dragged down their GDP.

India’s inflation went up, while Singapore posted good GDP numbers. Most economies appear to be softening with PMI and Services PMI moving into contraction.

Regionally, Australia’s inflation expectations remain elevated and immigration is running at quite high levels. While in New Zealand the pile on continues.

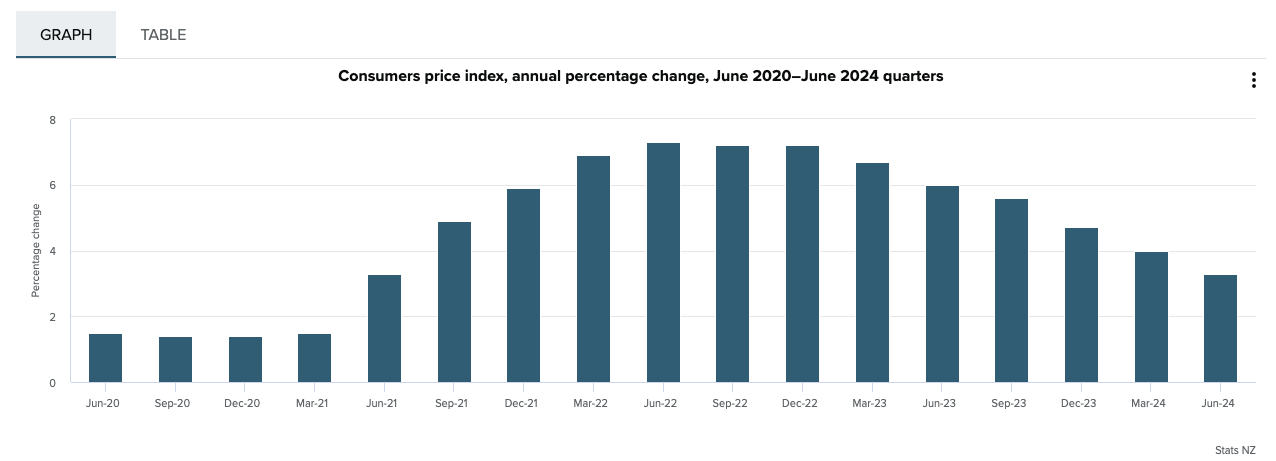

There was good news as food prices fell, but retail and housing are getting hammered, while PMI and Services are in free fall. No surprises then that the Q2 CPI result was under the RBNZ’s forecast at 3.3%.

Even the sticky non-tradable number fell substantially so the hopes of a rate cut in November are up. A polite reminder that the RBNZ wants to see CPI in the 1-3% range so we are still above target.

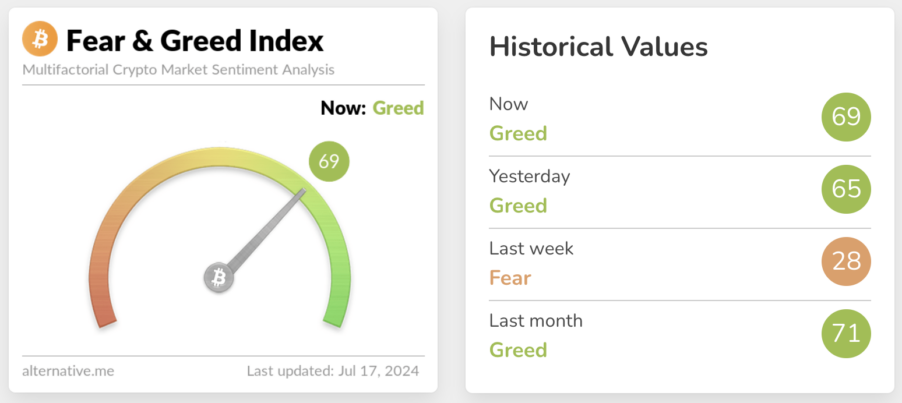

That pain you have in your neck is whiplash caused by watching the crypto market sentiment movements. We bounced from fear last week back into greed territory.

Highlights this week:

- Welcome back to a lot of green! Everything in the top 30 posted gains this week, some modest, while others like NEAR and XRP posting >30% weekly gains. Sentiment is a fickle mistress.

- Buy activity for the week was very high by value, meaning you saw the dip as discount season. Well played!

- BTC was the most bought asset. SOL was in the number 2 spot beating ETH and stablecoins by volume. Surprising and interesting!

- At the time of writing BTC, SOL and ETH were neck and neck, all up ~12%. XRP had a belter up 33%.

- Worldcoin (WLD) was our best performer this week, up 50%! STX was the best performing major, up 40%.

- MultiverseX (EGLD), was our worst performer, down 1% after last week’s break out.

View all top gainers: Visit the top gainers page to find out more.

Highlights from the crypto space

BTC continues to hold key support levels and ETF inflows are back into positive territory. The German government wallet has been emptied according to Arkham. $170m in shorts were liquidated because of the price rally over the weekend too.

Bloomberg’s senior ETF analyst predicted Spot Ether ETFs would start trading by July 23. The SEC is now re-evaluating drafts from potential Ether ETF issuers, delaying from the earlier expected date of July 18. Citi analysts are forecasting $4.5-5.6bn in AUM in the first 6 months.

Donald Trump selected pro-crypto Vance as his running mate for the 2024 election. It will be interesting to see how crypto’s influence unfolds in the US presidential race.

PayPals PYUSD stablecoin has reached a $500m market cap due to volumes on Solana.

Milk Road analysis into crypto points to APAC growing at a very healthy clip.

BlackRock’s BUIDL, its tokenized liquidity fund, continues to grow with AUM currently sitting at $460m. Goldman Sachs is reportedly going to launch 3 tokenisation (RWA) projects this year too.

And there is interest from both in MakerDAO’s $1bn tokenised Treasuries play.

Bitmex has pleaded guilty to flouting AML rules in its DOJ case. While the SEC dropped its case against Paxos for issuing BUSD.

Binance’s latest proof or reserves report states they have $115bn of assets on the platform.

NYDIG research out this week shows that while BTC had a poor Q2, being down 12%, it is still the best asset year to date.

Craig Wright faces a criminal investigation for lying and perjury… shocker! .

🌎 Macro news TLDR: …US CPI on track.

A Eurasian consortium, the Shanghai Cooperation Organisation, which represents 40% of the global population (but not India) held a summit last week to discuss a security alliance and de-dollarisation.

The shipping container index price plateaued this week, however remains extremely high.

The IMF expects the global economy to grow 3.2% in 2024

U.S. economic news

The Chairman of the Federal Reserve essentially pushed back on both political parties saying the Fed will make the call on rates using the available data regardless of the election cycle.

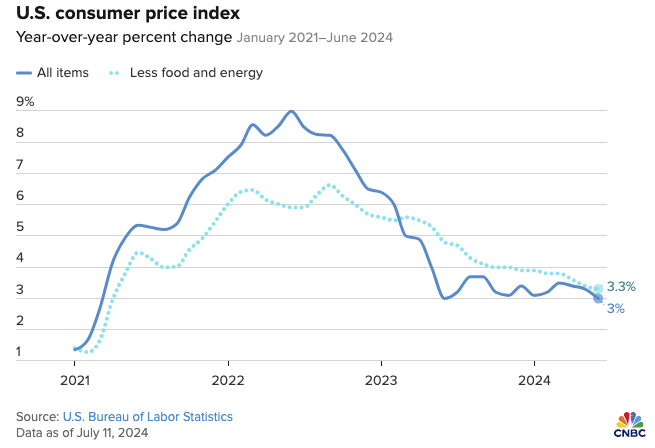

The big news of the week was the US June CPI reading. It was good! Better than expected saw monthly inflation falling 0.1% and annual inflation coming in at 3%.

Falling petrol prices helped. Core CPI was also better than predicted at 0.1% monthly and 3.3% annualised versus the 0.2% and 3.4% expected.

US PPI was 0.2% for the month and 2.6% annualised. That’s good too! CME fedwatch predictions tool today is showing an 85% chance of the first rate cut in September.

Over in Europe….

UK GDP for April surprised to the upside coming in at 0.4%. Britain is also loosening up regulations to enable more company listings so it can compete with the NYSE and Europe.

Germany said its CPI fell to 2.2% for June.

VP nominee Vance is a staunch American first supporter, and that could be bad news for Ukraine and Nato.

And in Asia Pacific…

China’s June CPI was 0.2% which was below expectations and means they continue to flirt with deflation. PPI is -0.8% due to excess capacity, in short the world’s manufacturing centre is making more than what the world wants.

Institutions are buying up Chinese bonds, and are in effect betting against the Chinese economy growing. Turned out to be a good bet; GDP missed forecast by quite a margin at 4.7% vs the 5.1% expected, dragged down by its property sector.

Singapore’s Q2 year on year GDP was 2.9%. India’s inflation rose sharply in June, up 1.1% to 5.6% annualised. Most of that is in food inflation running at over 9%. Wholesale prices are also up.

Australian consumer inflation expectations fell slightly, but at 4.3% are very high. Immigration is still running high as well.

In New Zealand…first the good news, annual food prices have declined for the first time in 6 years, down 0.3% YoY, and the latest Global Dairy Auction showed some strength.

Then it all goes south in a big way. Retail continues to take a battering, with electronic card spending down 3.7% in the June quarter, and down 5% year on year. Residential house sales volume is down 25% in June last year. PMI, as measured by BusinessNZ, tanked falling from 47.2 in May to 41.1 in June. Services PSI is even worse at 40.2.

Q2 CPI to June came in at 0.4% for the quarter and 3.3% annualised, down from 4% at the March reading. Last quarter’s area of concern was non-tradable (domestic) inflation, however this fell to 5.4% from 5.8% and was only up 0.9% in the quarter. All of this is better than forecast by RBNZ which had 3.6% in its latest monetary policy statement.

That’s a wrap for this week.

Stay tuned for the next update.

Did you miss the last weekly update?

Share to

Stay curious and informed

Your info will be handled according to our Privacy Policy.

Table of Contents

We make it easy.

Start your crypto journey today!

Make sure to follow our Twitter, Instagram, and YouTube channel to stay up-to-date with Easy Crypto!

Also, don’t forget to subscribe to our monthly newsletter to have the latest crypto insights, news, and updates delivered to our inbox.

Disclaimer: Information is current as at the date of publication. This is general information only and is not intended to be advice. Crypto is volatile, carries risk and the value can go up and down. Past performance is not an indicator of future returns. Please do your own research.

Last updated July 17, 2024