LUNA Collapse: What exactly happened?

How did the LUNA ecosystem collapse? Here is a painful truth about what happened.

Collapse blog cover")

At one point, Terra (LUNA) ranked as the 9th largest cryptocurrency in terms of market capitalisation at US$ 30 billion. It was a rising star at the beginning of 2022.

On 30 April 2022, Terra (LUNA) coins were valued at US $78 per unit. After a series of unfortunate events, in less than one month, LUNA lost 99.99% of its value at worst.

This has left many investors very confused and distressed. It must have been a shocking blow for those who outright believed in LUNA’s value proposition. There were also individuals who had their entire life savings completely vanish as they were invested heavily into LUNA alone.

Still others with some degree of exposure to LUNA must have felt angry about the sudden loss of their investment value, and sought out for answers.

You are reading the 2022 Crypto Winter Journals, a series where we uncover why the crypto market crashed in 2022, and what we can learn from it.

Why should we learn from LUNA’s collapse?

LUNA’s collapse was incredibly shocking to everyone in the crypto industry.

On paper, the fundamentals looked solid as Terra’s line of stablecoins had some use in several countries, such as South Korea and Mongolia. It has gained a positive reputation as a promising network with satisfactory levels of utility.

It would be very convenient to believe that there was an attack on the network by malevolent actors. Some big holders of LUNA may have believed so, and may continue to live in fear of the crypto world, knowing only half the truth.

The truth is that there was a combination of internal failures, triggered by external market forces and actors. The interplay between all the different factors are very complex. I could never do justice with a simple explanation to cover all the moving parts involved in this large-scale ecosystem collapse.

Still, it is important to face the truth and learn from it.

Crypto is neither good nor bad. It is simply a technology that is going through the growing pains of adoption. Fatal flaws in a system, if any, would still exist if we don’t have the ability to foresee them.

Terra stablecoins destabilised by selling pressure

An important point to note is that Terra’s ecosystem is built around the Terra stablecoins, among which is the famous UST token, which attempts to maintain a 1:1 value ratio (i.e. to be pegged) with the US dollar.

UST isn’t like other stablecoins. It is not backed by cash assets (like Tether and USDC) or digital assets (like Dai).

Instead, it relies on an algorithm that rewards arbitrage traders for maintaining the price of UST as close to $1 US dollar as possible. Terra’s native cryptocurrency LUNA is used as a kind of price volatility absorber, which the system heavily depended on.

The algorithm looks solid in theory.

If 1 UST is worth more than a dollar (say $1.05, or 5% more expensive), arbitrage traders can burn $1 worth of LUNA in order to mint exactly 1 UST. This 1 UST can then be sold to the open market, which is still worth $1.05.

In effect, the trader makes 5% of profit since it costs them $1 to mint 1 UST and they gain $1.05 after selling UST. Selling UST increases the supply of UST in the market, which lowers the price of UST.

The opposite case is also applicable.

If 1 UST is 5% cheaper at $0.95, arbitrage traders can burn 1 UST in order to mint exactly $1 worth of LUNA. That same amount of LUNA can be sold for $1. This means that the arbitrage trader can take something worth $0.95 and turn it into another that’s worth $1.00, gaining 5% of profit.

If arbitrageurs buy UST on the cheap in order to mint LUNA, theoretically, the price of UST goes back up to $1.00 as it becomes rarer in the market.

The system was running well when LUNA’s price was generally in an uptrend. However, when LUNA’s price slid down violently as UST was valued under $1, things got out of control in what experts call a “death spiral”.

How this death spiral looked like:

- Essentially, as 1 UST was cheaper than a dollar, the price of minted LUNA was still falling. This prevents arbitrageurs from making money off the trade.

- In turn, this caused arbitrage traders to lose interest in buying UST, thus failing to reduce the supply of UST to make it more expensive.

- When UST was under $1 for too long, UST holders lost faith in the stablecoin, causing them to sell — which further decreases the value of UST.

- Meanwhile, LUNA continues to be minted by the algorithm in an attempt to rescue UST from further devaluation. The increasing supply of LUNA in the open market causes the price of LUNA to go down further.

The negative feedback loop continued until LUNA was a fraction of a fraction of a penny. UST, too, would de-peg from its 1:1 ratio as it deeply depends on the market demand for LUNA.

Now, if you have carefully read the Terra whitepaper, and did a ton of research on the asset, would you have spotted a flaw in the design of the stablecoin? I doubt it, because very few people did.

The whitepaper illustrated how Terra works under ideal conditions. That is, when UST and other Terra stablecoins are used as medium of exchange, and when LUNA is held as a global store of value, much similar to what bitcoin is to many investors today.

Of course, nobody could have suspected (or perhaps dared to imagine) that over a few days, UST holders just sort of “gave up” on the stablecoin. This is the natural work of the market, but then again, another factor comes into play — Anchor Protocol.

Anchor Protocol reserve drying out

Anchor Protocol can be considered as Terra’s principal “crypto bank”. At one point, it was home to 72% of all the UST in the ecosystem.

Anchor also promises its depositors with nearly 20% yield per year. So, no wonder that UST holders were far more interested in saving UST on Anchor.

Of course, critics have argued that such a high interest rate is unsustainable. The high yield certainly helped increase the popularity of Anchor Protocol. During the height of the crypto market, Anchor also had borrowers who took on collateralized loans.

This meant that Anchor could theoretically maintain a healthy balance in its reserve to pay back users, even if some borrowers defaulted on their debt. On the contrary, however, Anchor Protocol reserves actually dwindled.

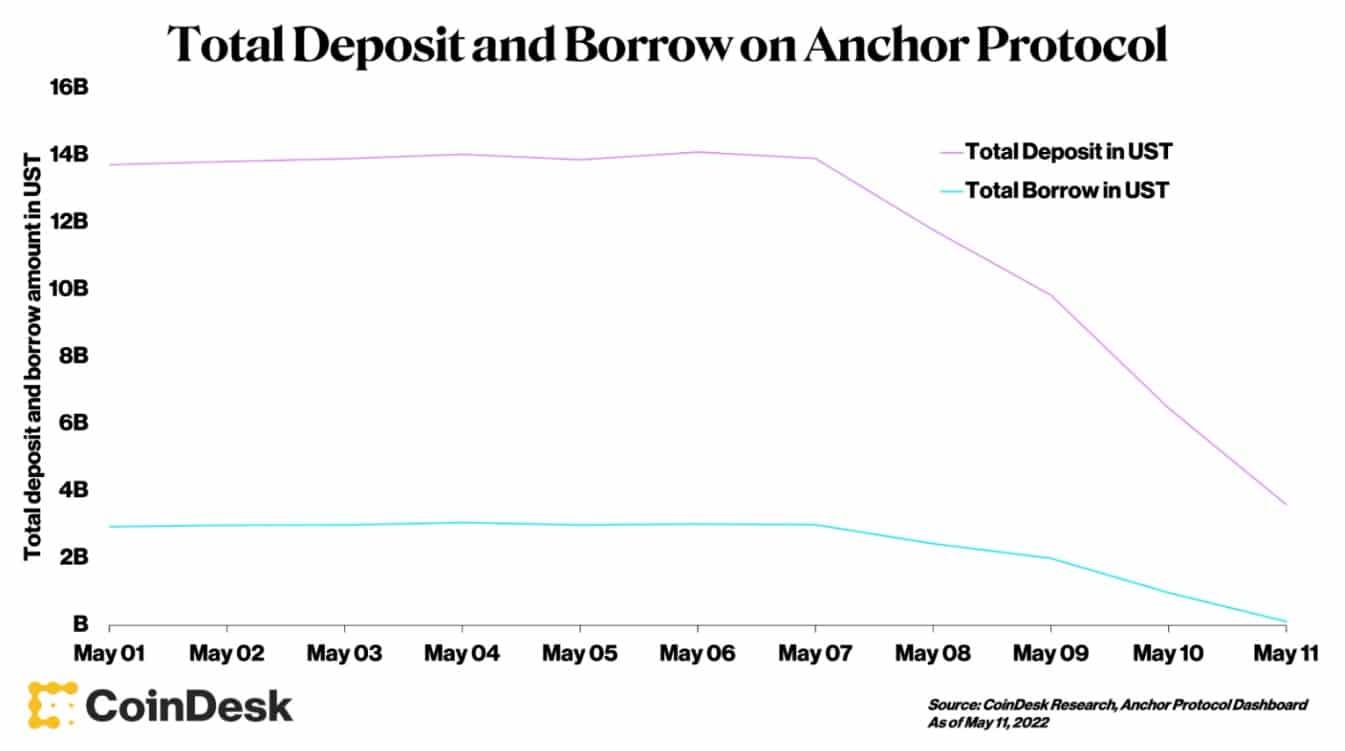

On-chain analysis shows that Anchor had to pay out the 20% yield to users from their own reserve. This is because during the bear market, there weren’t many borrowers, yet the number of deposits continued to increase.

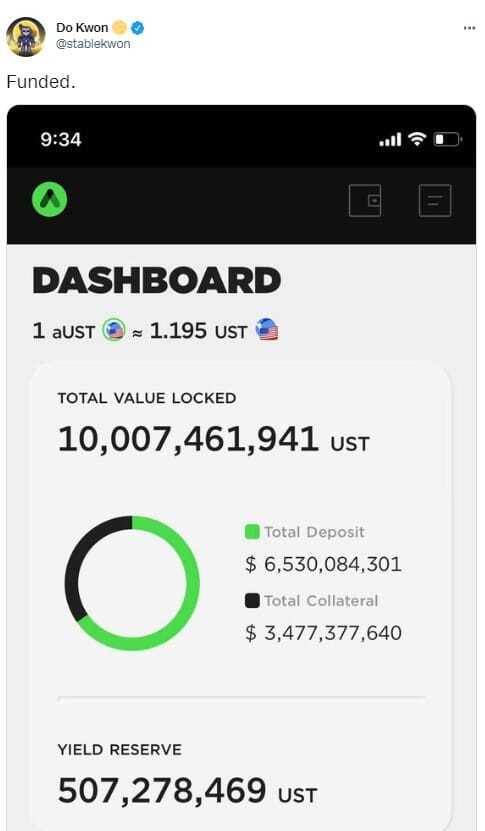

Anchor wasn’t making enough money to fulfil their lofty promises, but to no one’s surprise. Terra’s founder Do Kwon displayed publicly his attempt at calming down his followers, by “funding” the transparent Anchor Protocol reserve.

Many believe that Anchor’s low-risk high-reward yield (exclusive to UST) is the only strong reason why many investors flocked to buy UST.

If that 20% yield were to be reduced, as proposed in March 2022, following the reserve crisis, how many depositors would withdraw their funds?

In retrospect, the yield rate readjustment did not cause billions of dollars in bank runs. Rather, it was the work of another death spiral.

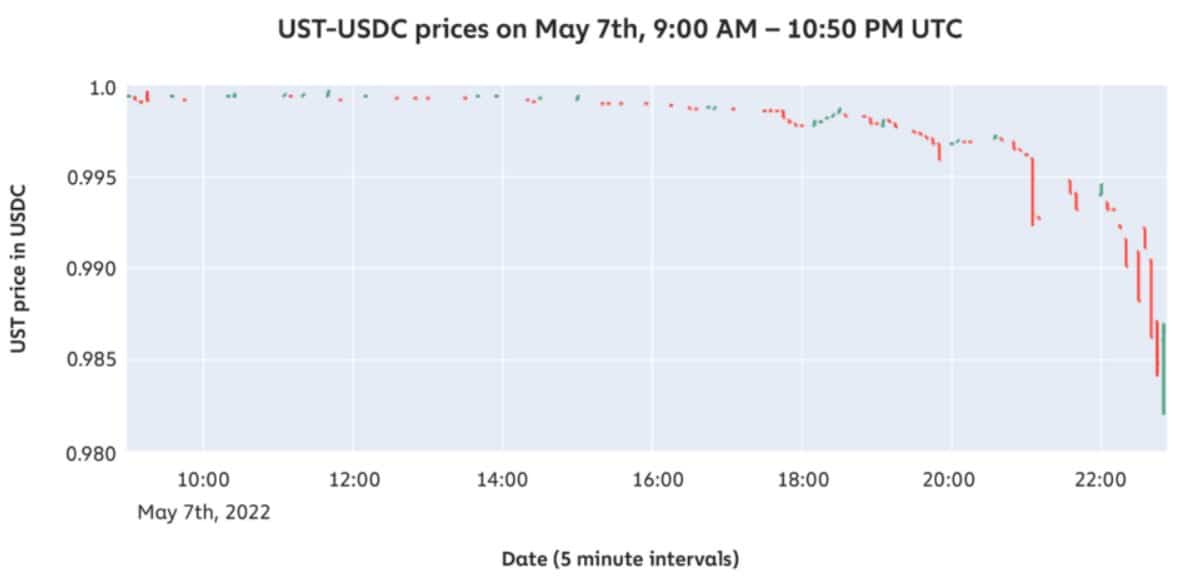

Starting 7 May 2022, billion dollars worth of UST were withdrawn from Anchor Protocol as a result of fear of a potential UST/USD de-pegging. The mass withdrawal caused a great selling pressure of UST, driving down the price of UST in effect.

As UST continued to de-peg, billions more UST were being withdrawn from the Anchor Protocol. Recall that a bulky majority of UST in circulation were stored in Anchor.

What enticed depositors to park their UST in Anchor, which gave UST and LUNA their short-lived success, had backfired and helped destroy the Terra ecosystem.

Allegations of a “financial attack”

All this death spiral would not have been triggered had an alleged “financial attack” not occur.

I say “alleged” because there were many sides to this story. That said, the “financial attack” may not actually have been an attack, but rather a series of logical moves by market participants.

The following chronology is taken from a detailed report by Coindesk.

It started on 13 March 2022, when Terra’s founder Do Kwon had a Twitter-based argument with a few major big accounts, such as Algod and GiganticRebirth. The two claimed that UST/LUNA is a Ponzi scheme, and collectively bet $11 million that the price of LUNA will be below $88 by March 2023.

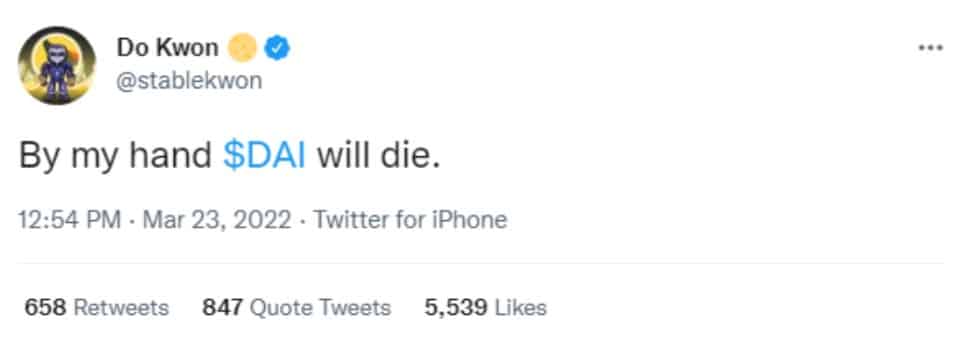

At this time, you should know that many people do not like Do Kwon for his arrogant and demeaning behaviour on social media. Here is one such example.

On 23 March, Do Kwon tweeted “By my hand DAI will die“, also a reaction to a claim that UST/LUNA is a Ponzi scheme, this time by Maker DAO’s cofounder. Do Kwon then publicly announced that he would be deploying a liquidity pool (decentralised swap protocol) called 4pool.

Do Kwon said in a tweet that 4pool is going to “starve” one of DeFi’s deepest liquidity pools called 3pool, which contains USDT, USDC, and DAI stablecoins. Do Kwon wanted 4pool to contain the aforementioned stablecoins except for DAI. 3pool is allocated in Curve Finance.

If this plan ever comes to fruition, in theory, 4pool would outpace 3pool’s growth. Excluding DAI means there could be a lower demand in the stablecoin.

Throughout April, the road was smooth for LUNA as its price was skyrocketing. UST became the third-largest stablecoin. On crypto Twitter, not many maintained their attention at the liquidity pool drama, but that would later unravel and mark the end of LUNA’s era.

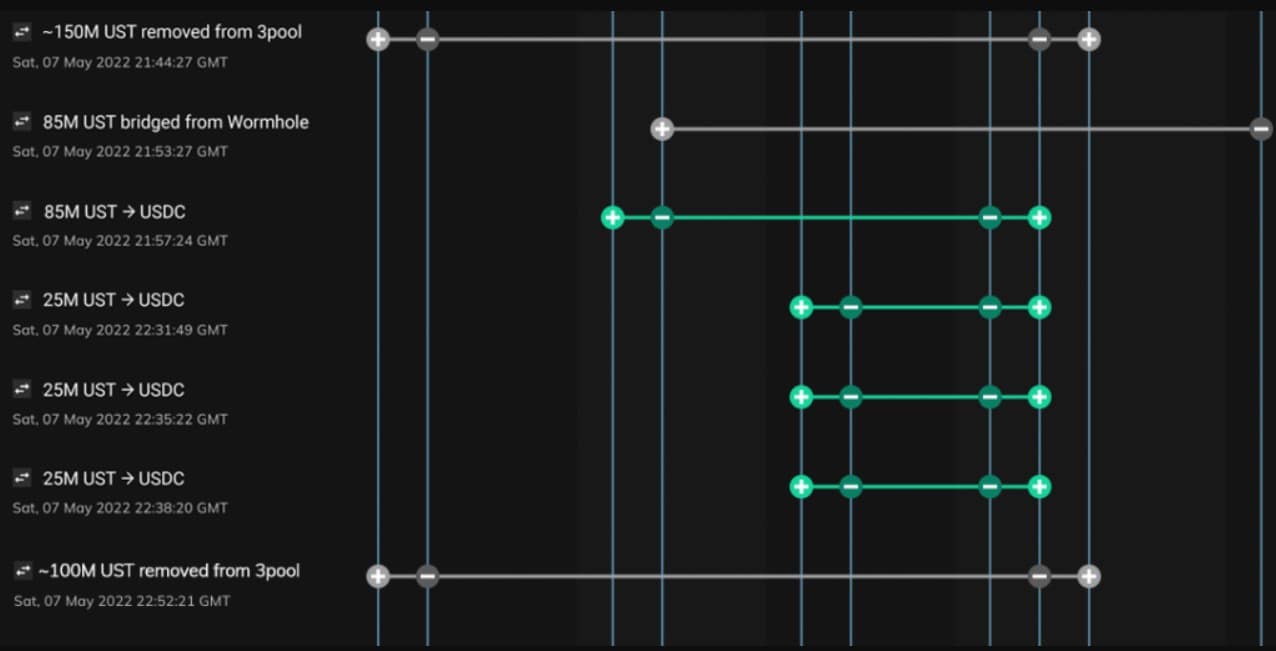

On 7 May, Do Kwon’s Terraform Labs withdrew 150 million UST from Curve’s 3pool liquidity pool as part of a planned and public operation. Removing so much asset value from an otherwise deep liquidity pool makes prices of UST in that pool more volatile.

According to Chainalysis (see above), after 13 minutes, one trader took advantage of this volatility and converted 85 million UST to USDC. Another trader also took advantage of this arbitrage opportunity to convert 100 million UST to USDC.

Curve’s liquidity pools automatically determine the prices of asset pairs (e.g. UST/USDC) by calculating their relative supply ratios. At this point in time, there is a 185 million USDC-UST imbalance, with the pool receiving too much UST at one time.

This causes UST to be worth less than USDC, in other words, UST is no longer 1 dollar, as USDC remains 1 dollar (in another pool).

The UST’s de-peg lasted 10 hours before three unidentified wallets swapped a combined $480 million USDT for UST in a span of three days. This was seen as an effort to restore the depeg.

On 9 May, the Luna Foundation Guard (part of Terraform labs), who in April had amassed billions worth of bitcoin (BTC), swapped them for UST in a desperate attempt to save the UST.

You could see from Tradingview that UST experienced a supply shock on that date.

Although UST’s price had increased for a brief time, the peg did not hold for long. Soon after, UST holders panic-sold the stablecoin on exchanges. Many UST holders, still believing in the algorithm, burned UST en-masse to over-mint LUNA tokens in an attempt to defend the peg, or to profit from the arbitrage.

This caused LUNA to go into hyperinflation, which degraded its value. Afterwards, the spiral of death ensued as the market cap for LUNA is well below that of UST. This meant that there is not enough dollar value in LUNA to make up for the loss of value in UST.

Just less than a month before its collapse, UST’s soaring demand propped up LUNA into the spotlight. When UST came crashing, so did LUNA.

What can we learn from this?

1. Understanding the technology

The first lesson in investing is to truly understand what we’re investing in.

Every single crypto project nowadays promises to 1) revolutionise money, 2) disrupt traditional finance, 3) change lives for the better.

But many projects fail to explain how they are going to set out to fulfil their virtuous missions. Very few of them can make people understand why their project is necessary. I even have a hard time understanding whitepapers and documentations.

Many investors do not come from a finance or computer science background. Neither do I, but lucky enough I was passionate about technology. This gave me a bit of a clue as to what problems could be solved with new technology.

Nowadays, I go straight to the documentation. I look at what programming language is being used by the blockchain, and see whether it’s easy to build something on that blockchain.

Think about this — if it’s so difficult to code a simple website, would Facebook, Twitter, or Google even exist (or exist for free?). A blockchain is only useful if anyone can easily build on it.

2. Watch out for low-risk high-reward schemes

Crypto’s high volatility can help traders make a decent amount of money with relatively small capital. However, this doesn’t mean that crypto is a magical land where money grew out of the ground like mushrooms.

Anchor’s 20% stable annual yield should cause some alarm. If 20% is given to depositors, then Anchor should charge borrowers with much higher interest rates, wouldn’t it?

But the opposite is true — borrowers are rewarded with Achor’s ANC token for borrowing UST. They were getting paid to borrow, so where did the extra money come from?

Also, if you have had experience with trading cryptocurrencies in all market conditions, you should know that trading in a sideways and bear market is much harder to do than in a bull market.

Making money in such conditions is hard, so why should Anchor guarantee a 20% stable annual yield?

3. Diversify across many different projects

No matter how deep you understand the technology, or how much you’ve done your research to avoid getting into risky schemes, some things are out of our control.

Diversifying across different cryptocurrency protects us in the unlikely event that one fails just like LUNA.

If you’ve been investing in crypto for a while now, you should have already experienced the benefits of diversification. On one hand, one coin may be rising in price faster than all the rest, which allows you to earn potentially higher returns.

On the other hand, coins that are less volatile could protect you from quickly losing your investment value if a coin turns out to be a failed project.

4. Learn to manage risk first before making money

Too many people forget that crypto is a risky asset. They would prioritise learning how to make money, and finding places to deposit for the highest yield returns. Alternatively, they’d scour the Internet for potential coins that can multiply in value over a short time.

“Managing risk” sounds boring indeed. But it’s the first thing that anyone should learn about, before risking billions of dollars of your or other people’s money. Hedge funds and crypto banks, out of all people should know this.

Unfortunately, Three Arrows Capital, Voyager, and Celcius, are three of the names who fell the hardest for ignoring this rule. We’ll talk about these in the next article.

Stay tuned.

Share to

Stay curious and informed

Your info will be handled according to our Privacy Policy.

Table of Contents

We make it easy.

Start your crypto journey today!

Make sure to follow our Twitter, Instagram, and YouTube channel to stay up-to-date with Easy Crypto!

Also, don’t forget to subscribe to our monthly newsletter to have the latest crypto insights, news, and updates delivered to our inbox.

Disclaimer: Information is current as at the date of publication. This is general information only and is not intended to be advice. Crypto is volatile, carries risk and the value can go up and down. Past performance is not an indicator of future returns. Please do your own research.

Last updated November 21, 2022