Weekly Market Update: Shanghai was a success

In this weekly market review, we take a look at post-Shanghai and highlight other macro economic and crypto developments from around the world.

The macro view this week points to a softening of the US economy as their inflation appears to have peaked. Markets are predicting one more 25 Bps rate hike in May.

Europe looks like it has more work to do on its inflation, while China’s post Covid rebound looks firmly underway.

However, the news for the rest of Asia and Australia is mixed, although the signs are leaning more positive.

New Zealand looks increasingly like an outlier currently due to the pressures caused by the impacts of our January weather and a potential wage spiral.

🌎 Macro news TLDR: Signs of global softening.

Crypto markets are looking particularly strong at present, especially post the Ethereum Shanghai/Capella upgrade. The signs of a bear market seem to be dwindling by the day.

Starting off with global news

The IMF is predicting 3% global growth for the next 5 years, the lowest since 1990. China’s ability to be the global growth engine is fading, mainly due to saturation and population dynamics.

U.S. economic news

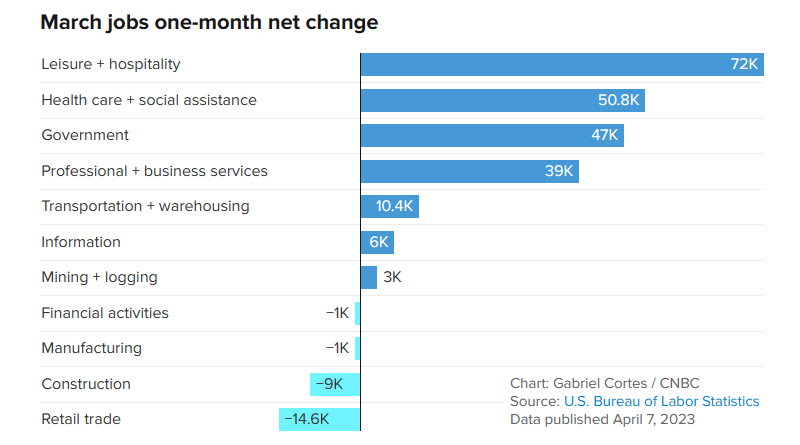

US jobs data shows that available positions have fallen below 10 million for the first time since March 21.

Job openings are persistently high, however most of the additions are in lower paid sectors which is curtailing wage inflation.

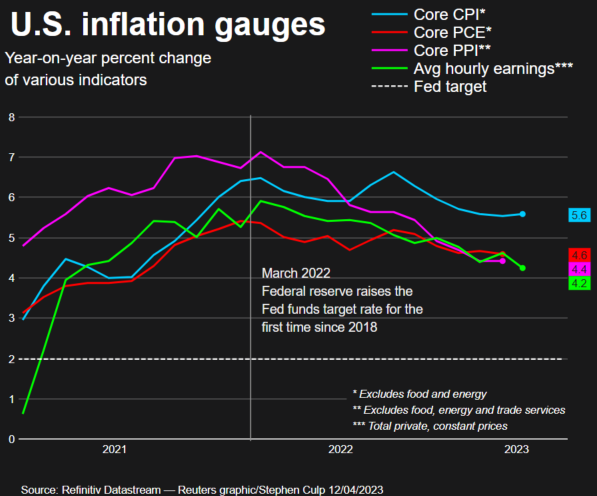

US CPI growth continued to slow, increasing by 0.1% for March. However, that good news was offset by a 0.4% increase in Core CPI which is now looking to be at 5.4% annualised.

The minutes indicate that the FOMC has no intent on easing their stance on inflation. Additionally, the Fed has now openly said the US may experiencea recession later this year, but blamed the banking crisis for that.

Adding to this confused picture, Produce Price Inflation (wholesale inflation) fell 0.5% for March. US retail sales were also down 1% indicating that the economy is softening.

Meanwhile, in Europe

The ECB is hinting that core inflation remains too high, meaning more rate hikes are likely.

Indeed one of their committee members has said that a 50 Bps rise may be in the pipeline for May; the consensus appears to be 25 Bps. European retail sales showed a continuation of a fall that started in 2022.

The UK economy flatlined in February, with industrial action across multiple sectors being blamed. Things look bleak with the IMF projections putting the UK at the bottom for growth.

In Ukraine news, Fighting in Bakhmut has been labelled unprecedented. The major economic impact still seems centred around grain supplies, with Russia threatening to cancel the Black Sea Grain corridor deal, which could increase global food prices by 15%.

Geopolitics continue to swirl with Russia-China ties looking like they continue to strengthen. Meanwhile Finland, who also shares a border with Russia, has joined NATO leading to speculation of a wider conflict evolving.

Moving on to Asia…

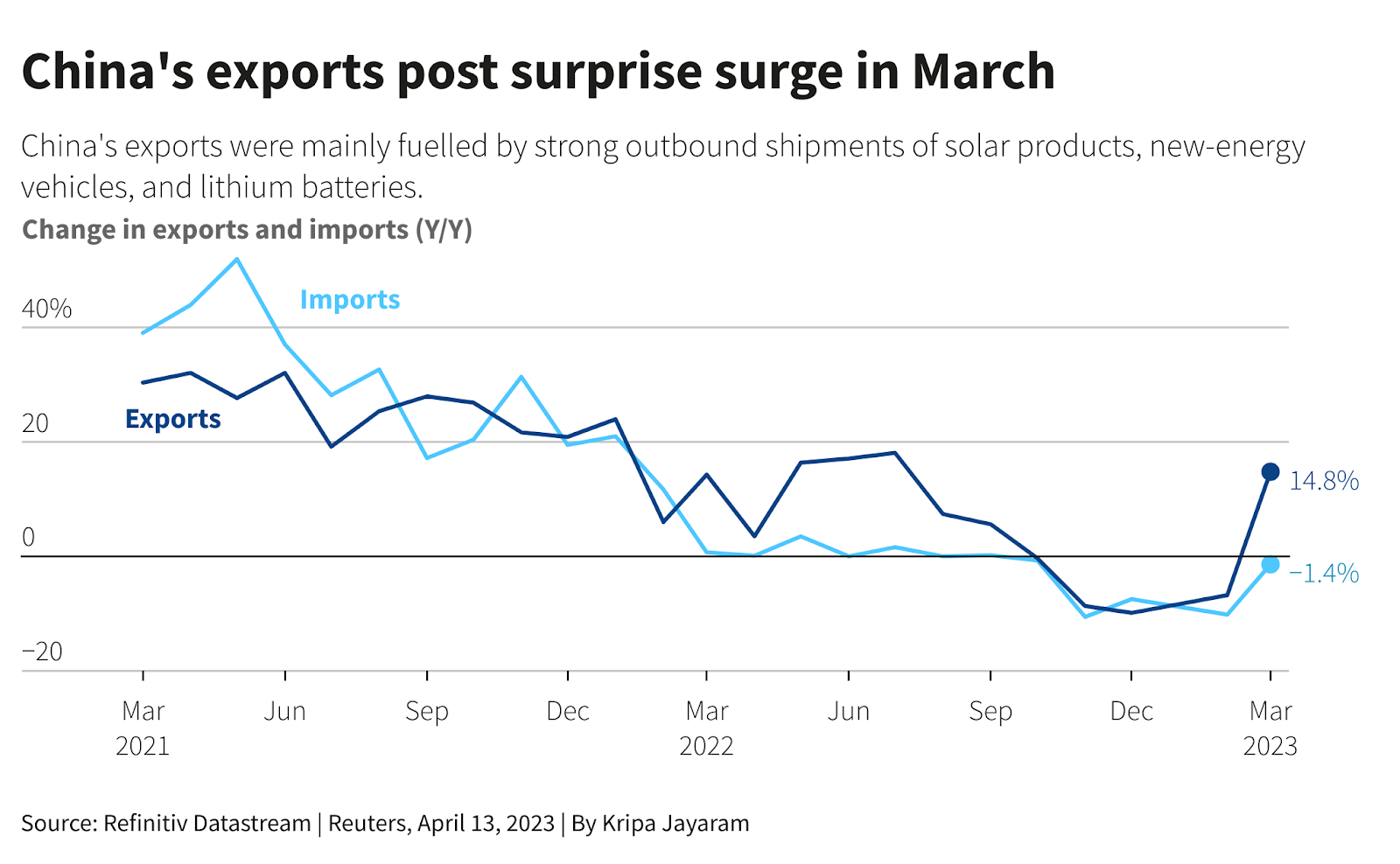

Chinese Consumer Inflation for March was only 0.7%, and is down on an annualised basis. Lending for investment is also picking up, and they had a great March with their export sector up 14%.

In response to Taiwan’s president meeting a senior US representative, China has undertaken 3 days of military drills around the island.

It’s worth noting that Taiwan’s exports fell for the 7th straight month, potentially due to reduced Chinese orders.

The Bank of Japan’s new governor has said he is going to hold the course on their ‘accommodating’ monetary policy. Similarly, India’s central bank has paused its tightening cycle as CPI is falling.

Singapore’s GDP for March surprised markets by falling 0.7% in Q1. In response the Monetary Authority has paused monetary tightening.

Looking to Australia, consumer confidence has spiked, potentially off the back of the RBA’s interest rate pause, while unemployment remains at a 50-year low.

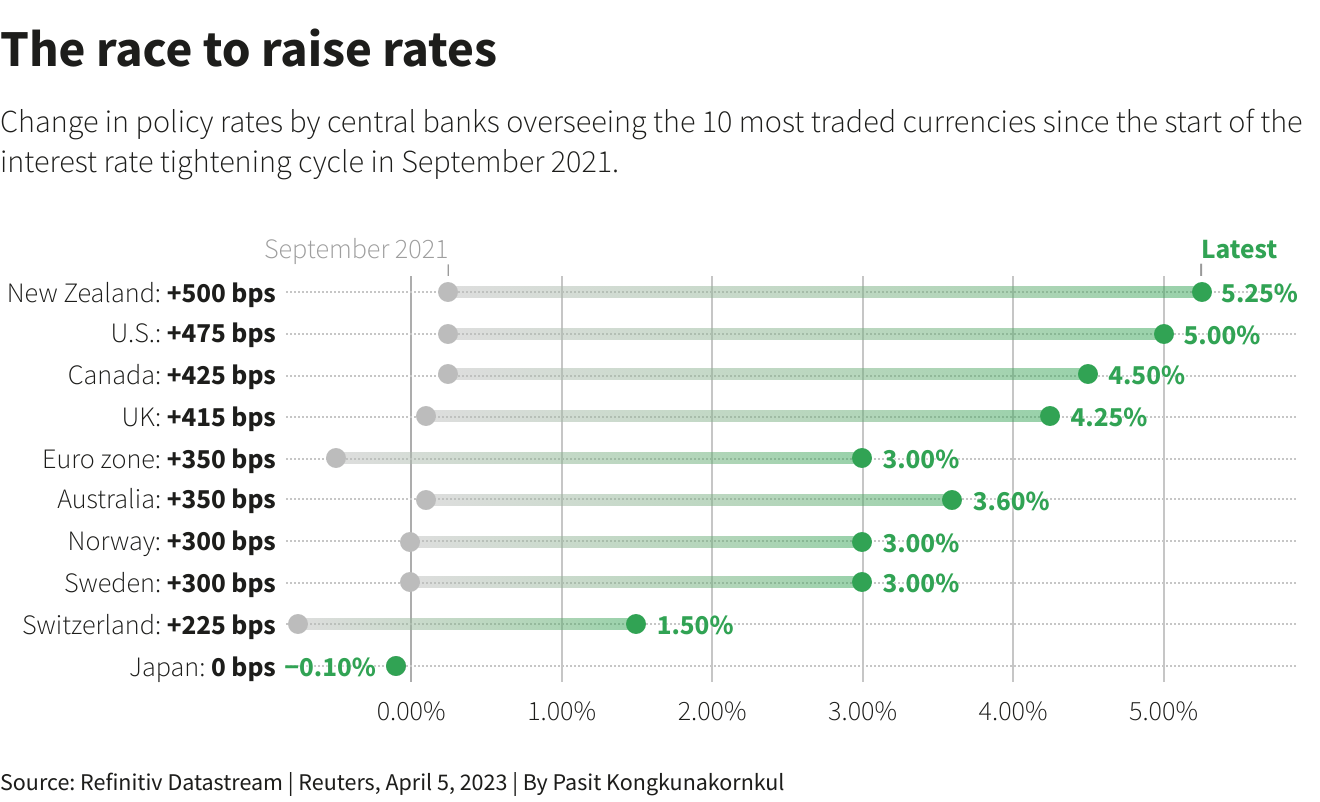

Finally, here in New Zealand, the RBNZ’s surprise 50 Bps OCR raise puts NZ in the lead to raise rates in the top traded currencies.

Meanwhile, our manufacturing sector contracted for Q1, with a PMI reading of 48.1.

Food price inflation for March was up 0.3% on February, however annualised food prices are up 12.1% year on year. A reminder, NZ CPI data comes out later this week with market expectations being around 7.2%.

Highlights from the Crypto Space

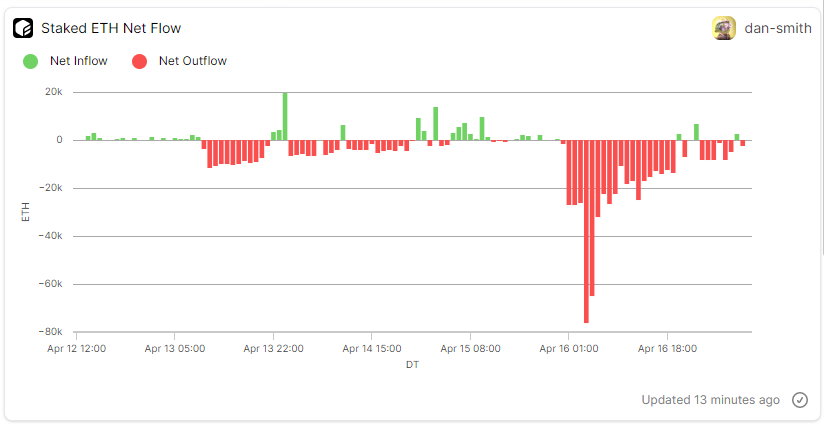

The Ethereum Shanghai Capella (Shapella) update was activated successfully which enabled validators to un-stake their ETH tokens and rewards, along with bringing other improvements to the network.

There were plenty of opinions on what would happen, and we appear to have our answer with withdrawals now clearly declining in volume.

Read more: What is the Ethereum Shanghai Update?

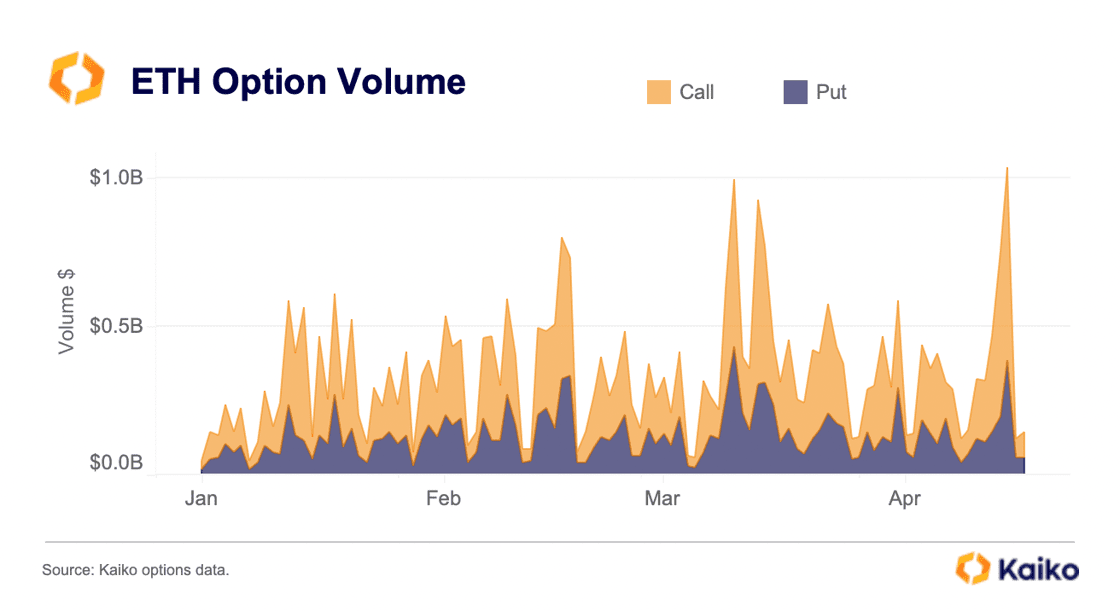

Forward looking options trading suggests that the market has gone long on ETH with Call options hitting a mult-year high according to Kaiko.

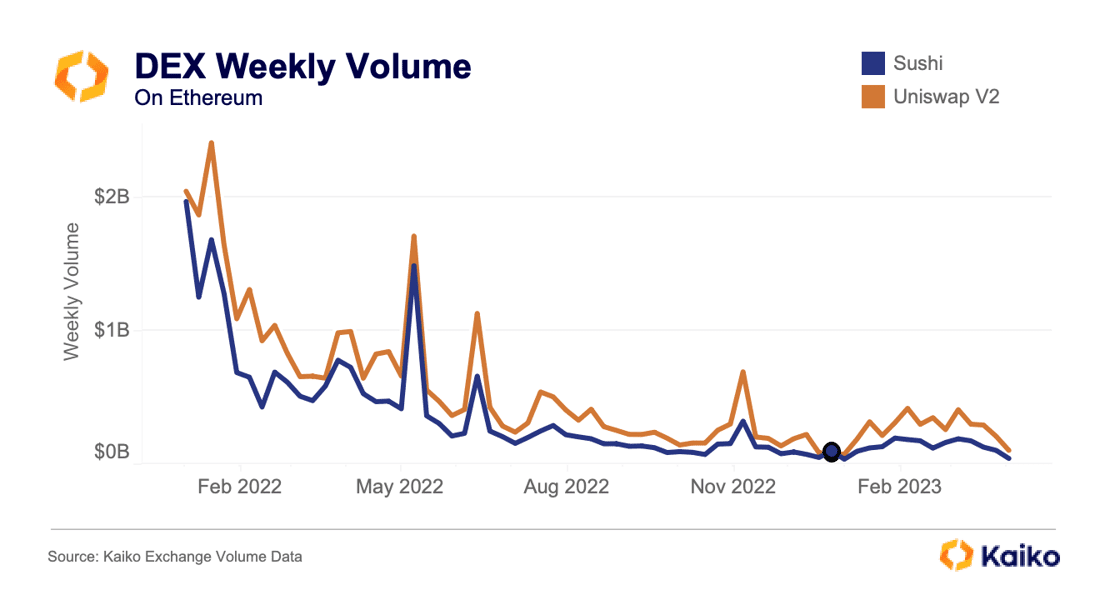

Uniswap seems to have been a beneficiary of the US regulatory crackdown with its volumes way above Coinbase. Sushiswap on the other hand is trending in the wrong direction.

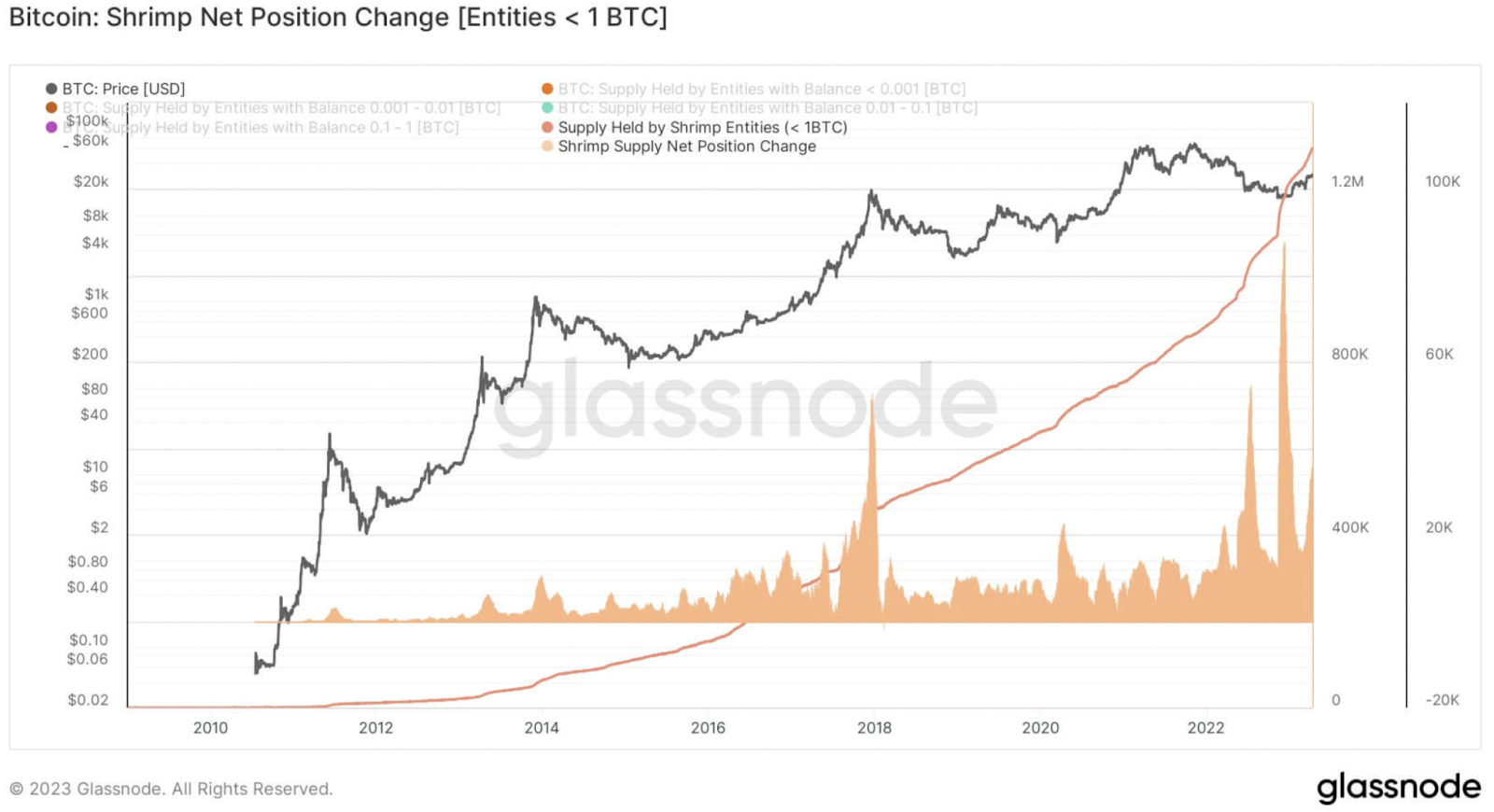

So-called Bitcoin Shrimp wallets (<1BTC) have been aggressively accumulating BTC in the last month, adding 35,000 BTC to 1.3m.

Hong Kong’s finance chief reiterated their position that they are open for crypto business. Meanwhile, the US SEC has now set its sights on DeFi. However the tide may be turning on Commissioner Gensler with a Congressman putting forward a bill to have him removed from the SEC.

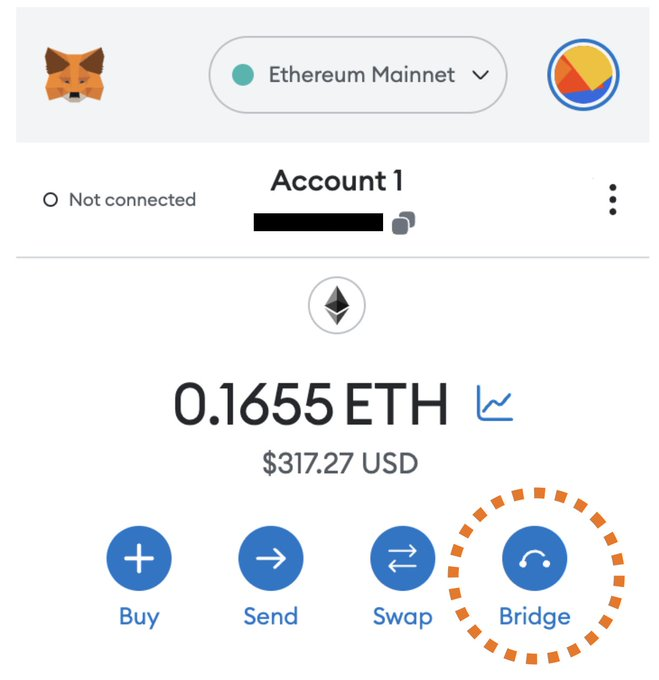

Metamask has added a bridge function which supports Arbitrum, Polygon, Optimism, Avalanche, BSC and Ethereum – making it easier than ever to facilitate multi-chain transactions.

Other updates from around the crypto space:

- Elon Musk is being sued for $258bn for his DOGE coin tweets. Ironic Staying with Twitter, eToro looks set to offer its social trading services to Twitter users.

- Paxful, a P2P exchange is shutting down.

- Moon Mortgages launched a mortgage product allowing you to use crypto as collateral in some states in the US.

- Two former Gemini execs who have tokenised US treasuries in a move that makes a lot of sense.

- In Australia, ASIC has cancelled Binance Australia’s financial services licence, which means no more derivatives trading.

- The Winklevoss Twins are lending $100m to Gemini to help it through the winter.

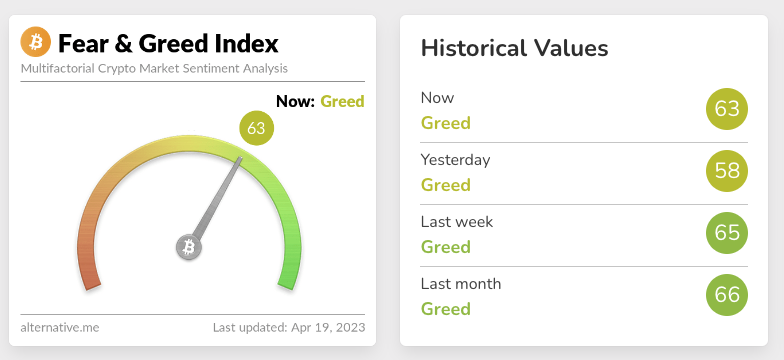

The sentiment in the crypto market remains static as we hold steady for the 3rd week in a row in greed territory.

It has been another very solid week in the markets with the majority of the top 30 assets showing gains. At the time of writing BTC closed the week up 2% while ETH was up another 9%. BNB was up by 7% and XRP was flat. SOL also had a great week, up by 18%.

Our biggest gainer this week was Render (RNDR) up by 40%. Stacks (STX) was this week’s biggest loser, down by 8%.

View all top gainers: Visit the top gainers page.

Looking for more flexible pricing and trading volume for your high-value crypto trades? Get in touch on our OTC page and learn how we can help.

Stay tuned for more weekly market updates!

Be sure to sign-up to our newsletter below and follow our social channels for the latest in all things crypto.

Did you miss the previous market update?

Share to

Stay curious and informed

Your info will be handled according to our Privacy Policy.

Table of Contents

We make it easy.

Start your crypto journey today!

Make sure to follow our Twitter, Instagram, and YouTube channel to stay up-to-date with Easy Crypto!

Also, don’t forget to subscribe to our monthly newsletter to have the latest crypto insights, news, and updates delivered to our inbox.

Disclaimer: Information is current as at the date of publication. This is general information only and is not intended to be advice. Crypto is volatile, carries risk and the value can go up and down. Past performance is not an indicator of future returns. Please do your own research.

Last updated April 19, 2023